Tweet is here: https://twitter.com/sama/status/636586179970752512

Still impressive though. Any success rate over say 10-20% seems really impressive for an incubator.

> If we don’t invest in these companies, they don’t happen… The thing about Y Combinator that’s cool is that most companies won’t happen if we don’t fund them.[1]

I thought YC was always looking to fund those that would exist with or without YC. I have seen less and less "crazy bets" every batch, but I have to say there's more diversity of founders and topics (biotech, energy, farming). Companies generate revenue before DemoDay and many are startups that work for other startups. It's not a bad thing but would love to see more Airbnbs or Reddits around. Those are the ones that can generate a true impact on society and can only exist thanks to YC giving them a chance. The fellowship can be a great starting point for those.

[1] http://venturebeat.com/2015/08/23/sam-altman-and-jessica-liv...

Well, they try to filter by that quality, as would any other incubator or investor. It would make no sense to accept apathetic founders who will surrender at the first obstacle. Personally, I'm skeptical that they having any advantage in identifying such abstract traits. How would you identify it from a 15 minute interview?

Though you do have a point; I would expect a higher failure rate from an accelerator given that they fund riskier ventures.

What I'd like to know is the value, at exit, of the companies that have exited or gone public. Because I can guarantee you that the "valuation" of $65B+ is a totally meaningless number. This includes every single company that had a huge, unsustainable up round which will almost certainly be devalued based on future financings or exits.

"Meaningless" is hyperbolic. How much would you pay for a share of Airbnb? More than nothing, I assume. I think one can conclude something from consummated, informed responses to this question.

A more interesting observation is that two companies account for over half of the $65 billion. Airbnb's most recent valuation was reportedly $25 billion, and Dropbox's was reportedly $10 billion. These companies are not likely to go away overnight a la Homejoy, but their valuations are going to be hard to sustain. Dropbox in particular would be a very tough sell to the public markets at its private market valuation given its comp[1].

Making analysis even more difficult is that today's big money, late-stage deals have lots of strings attached, so these valuations are hard to assess without knowing all of the details.

Final comment: despite the constant suggestions to the contrary, YC's portfolio appears to live in the very same power law reality as most early-stage investment portfolios in Silicon Valley.

[1] https://www.cbinsights.com/blog/dropbox-valuation-bubble/

There you got your response at the beginning of the post. It seems that you are attacking for the sake of attacking? Sam is providing these data because people asked for them.

For a bit more, dropbox & AirBnb are worth 10 & 25 billion. That's over half the total $65bn from 2/940 companies, 0.21%. Even if we assume these stats grossly underestimate ultimate valuations because of most of the companies are still young, it's still likely to end at >50% of value from <1% individuals. This is for companies that get into YC, which is already a select group.

Accelerators on the whole are a terrible business, and we try to be up front about that with everyone who comes to us for advice.

Is it YC's human resources, position in the market, branding, some combination?

These kinds of companies with massive bandwidth costs rarely become profitable, and even if Twitch bucks the trend, Amazon could easily use Hollywood accounting to avoid any payments on the earn-out (for example, it could charge Twitch retail rates for use of AWS services). It strikes me as a bad decision to accept an earn-out when the overwhelming likelihood is that the clause will result in exactly $0 going to the former owners.

Re: stats, 40 out of 940 are worth more than $100M. Dozens more are probably worth at least $25M. That is an insanely high success rate. The YC system works!

A fairly common outcome (anecdata from friends) is that the earnout is virtually in the bag at the 50% point and after that they are mildly frustrated with thumb-twiddling while waiting for the clock.

Meaning, if you are right about the business, these milestones are trivial to hit. If you don't accept the earn-out, it's a signal that something you are saying is either wrong or being misinterpreted.

I was wondering though, if the Fellowship program showed great results and you guys decide to continue it, how much equity would you ask for? Have you thought that far ahead yet?

Total Investment: ~$131,600,000 Total Companies Value: >$65,000,000,000 YCombinator's 7% Value: $4,550,000,000 Total Return: 3357% Annualized Return: 42.5%

Obviously, it costs more than the initial investment, but these are really nice numbers if compared to a mutual fund, etc. Did I make any mistaken assumptions?

https://blog.ycombinator.com/the-new-deal

From 2012-2014, YC companies received an automatic $85K follow-on investment from a syndicate of investors, though this was not funded by YC. From 2011-2012, they received an automatic $150K from Yuri Milner. From 2005-2011, it was $6K/founder (I think very early on, it was a flat $20K). So YC's capital expended has been a lot less over time than the current deal would reflect.

YC recently (1-2 years ago?) started giving 120k. Before that, it was 10-20k. So let's say half of what you said is the total investment = 65M.

That's a 10X return. I actually was expecting higher. Am I missing something in my numbers?

It still won't be 90% though, but YC companies are widely known to not be representative. It's the highest profile accelerator, so it attracts the best talent. Just like people who graduate from Ivy League schools earn more on average, but mostly that's because they attract people who are above average to begin with.

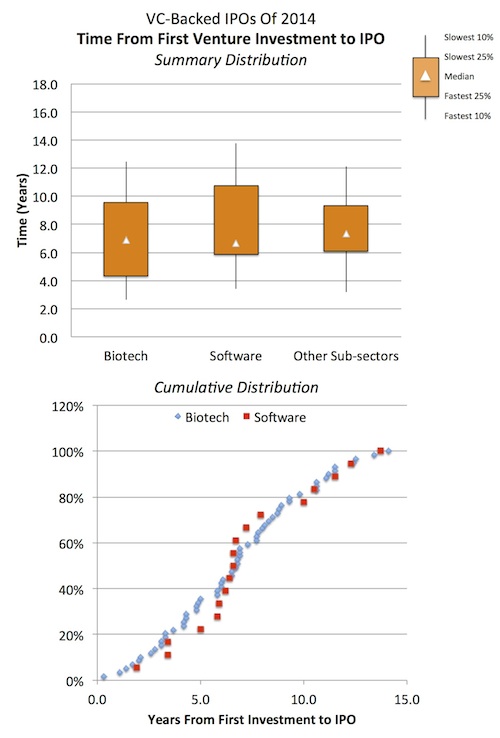

YC has been around for 10 years. Average age of a company from First Investment to IPO in 2014 is less than 10 years (http://lifescivc.com/wp-content/uploads/2015/02/Time-From-VC... Source 1.)

Personally, I believe startups excel when odds were stacks against us (forced to innovate and make founders strong and tested). I think YC or any incubator has a structure that shields companies from facing challenges initially.

I don't think Incubators are proven to be a great Idea yet ( if you are someone with industry experience rather than a fresh graduate).

1. http://www.forbes.com/sites/brucebooth/2015/02/24/tortoise-h...

Though, I do wonder, how feasible would it be to end up with a 2+mill nest egg(or however much you need to live off the gains) by ~35 and retire right then and there.

Edit: Forgot a word.

It would allow prospective applicants to think about whether to apply, and hopefully keep the pile a manageable size for the people reading it.

The numbers reveal that it's hard, but startups were ALWAYS hard. It's still the hardest thing I've ever done and most founders say the same. As far as YC is concerned, we don't want people to try to make this easier for us. One of the unique properties of YC is that we're trying to fund startups at scale and that means we don't want founders thinking about trying to make it manageable for us by bowing out. That's how I miss out on someone on the margins. It's one of the reasons why I love working on the YC software team to try and solve these challenges. So please, don't take away my work. :)

My favorite founders are filled with grit and perseverance. They don't calculate whether they can change the world before starting, they just start. So if you're ready to do something hard and feel like it's within you to change the world, please do apply...the numbers be damned.

Thats why fellowship experiment is going on, but I think you guys would have more time to read applications and "discover" great startups if you didn't encourage every steve-jobs-wannabe to apply.

just my 2 cents

Average people, that do average things, generally think in terms of the odds "what's my chance of this, or that.." when deciding about things.

Extraordinary people don't care about their chances, they do things because they are determined or obsessed about whatever it is they are doing, and stop at nothing to make it happen. These are the types of people that go on to build great companies and are the types of people YC generally looks for in the applications.

So if you're the type of person that doesn't care about the stats: you should definitely apply!

> Oh, another important stat: about 300 of the companies we have funded have shut down.

This is a hard gig. Even after you get into the top accelerator in silicon valley.

Does this include aqui-hires?

Also, would you know how many companies rejected by YC are worth more than $1 billion? Zero or non-zero? :)

Also, saying a company was acqui-hired makes a VC look less successful, so they have an incentive not to be honest about it.

I assume YC is doing great for themselves, so I'm wondering, what is the rule of thumb to say an investment was successful? (for YC, knowing they invest cheap and early.)

Is it once a company reaches 10M? 1M? Where there is an exit?

It would be interesting to know how many companies YC says the investment was a success (either made money or will if no exit yet).

The billion dollar number is freaking incredible. There are 115 venture-backed private companies globally that have unicorn valuations[1]. For 8 of them to have been through the same accelerator is amazing.

Sorry to be negative, but worth according to whom?

If none of these companies are public, the valuation comes from a very narrow group of private investors. In what seems to be a bubble (and an echo chamber) in S.V., these valuations may be vastly overstated.

That said, kudos to YC for being transparent.

Do you not think that solid data such as revenue, revenue growth and profit/loss (or at least burn rate) would be a much better measure of success? Some non-public companies (like Uber) publish some of these numbers.

If all of those companies wanted to exit at the price of their most recent raise, they wouldn't be able to. That means that at least some of the valuations are unrealistic.

Number of companies we offered to fund yesterday for the first YC Fellowship: 32

At a certain point you can only learn so much from other's failures but it would be interesting non-the-less.

airbnb dropbox stripe twitch weebly machinezone were all funded >5 years ago... Unicorns in the past 5 years are Instacart and Zenefits (there will surely be others). In general it is hard to measure performance of the entire portfolio, much easier to measure performance of a class.

Like kevin said elsewhere in the thread, it's about finding the amazing founders in the margins -- we want to see everything, and YC can still be a good fit for everyone.

Good to see the 90% of startups fail 'statistic' blown out the water with some facts!

If YC companies were representative of all startups there wouldn't be any point in going through YC.

But just remember that, even though these numbers look amazing, you can create a business via other means and still possibly achieve whatever sort of success you're after -- you don't have to join an accelerator, or get prestigious seed or venture funding.

Or at least, I think that you shouldn't have to.

Coolios.

I take it YC has some initiative wrt biotech and healthcare and I missed it (cuz I am busy)?

Also pretty incredible that they're over 100 in this last batch.

> Oh, another important stat: about 300 of the companies we have funded have shut down.

Not based on current valuation but based on actual exits and money returned to YC?

Wow.

Just wow.

The use of the term "market cap" is especially ironic given Sam's recent post on "financial misstatements"[1]. If founders are expected to use financial terms accurately and appropriately, shouldn't investors be expected to do the same?

{kind=link}