The one thing I believe people should know about the stock market is: There are people with more capital, time, and knowledge than you who will consistently beat you. Picking individual investments is mostly a sucker's game.

Buying tech stocks and/or crypto in the last couple of years has been a consistent exception to this, but I worry that many of the people who made good money from those investments will now believe that they have some superior understanding that lets them consistently beat the market. But sooner or later they will find themselves in a similar situation as those who thought investing in Japanese Tech companies was a surefire way to beat the market 20-25 years ago.

So my advice to anyone who already got rich from their investments in the last couple of years: Congratulations! Now take that money, invest it in the most boring thing possible, and enjoy life.

To everyone who is trying to get rich quick now: Do your thing I guess, but be aware that you're gambling.

1. Commodities are bad long term bets because technology gets better. I remember people talking my ear off about peak oil and then the US turned into a net-exporter. Short term inelasticity, yes can sky rocket prices; but long term prices go down.

2. Physics based thinking. I knew electric cars were going to work because the math checked out.

3. Economics of scale works. Find companies that understand this and focus on it. When I saw Telsa focussing on a single car for a year I knew they would be a winner.

4. Software scales. People like to make money. Combine the two and its a real winner.

5. Sell when forward price to earnings after cash starts to look wonky. Which was 2007 and I think 2019. Covid and the direct stimulus kinda messed up the timing, but the market is still completely screwed. Either way, sell early and buy the crash.

Telsa, Apple, Shopify, Amazon, Google. Only really lost on Etsy (I can't believe how much they missed the opportunity to become a real platform).

Why bother investing in GM through a broad index fund if I know for sure Tesla will eat their lunch?

This isn't really get-rich-quick. This is looking at companies rationally and projecting where they will be in a year or two. And rationally speaking this market is out of wack and I wouldn't advise investing in even my favourite tech companies right now. I don't think this is Japanese Tech level of readjustment. I think there will be a -%50 S&P500 crash, maybe more, and then in 10 years Apple will be worth more than double what it is worth today. They have fundamentally better technology. Their software competency is below average, but their hardware, fit and finish, design, and cultural cache is world class and it is hard for me to imagine any scenario where they lose other than a US war with China.

There were plenty of tech losers. You still had to pick the winners.

> Physics based thinking. I knew electric cars were going to work because the math checked out.

Electric cars were obvious, but Tesla was not an obvious play. In hindsight, it might seem so, but in the beginning it was far from clear that Tesla would dominate the space. Additionally, time will tell if Tesla's stock stays 8x higher than its pre-pandemic price.

> Sell when forward price to earnings after cash starts to look wonky. Which was 2007 and I think 2019.

This happened many more times than the two massive crashes. If you actually followed this advice, you'd probably be worse off than investing in the s&p - even if you did pick good stocks.

--

As others have mentioned, beating the market with $1M invested is much easier than beating the market with $10B invested. Especially when your appetite for potentially losing money is much higher.

Let's naively assume that you actually can pick stocks. At $10Bn - you need to pick more stocks - otherwise you would drive up the price too much in buying that much of the stock - unless you only picked Apple and Google and MSFT and Amazon.

Tesla's stock price isn't really related to the fundamentals. It's a meme stock that, as you note, benefited hugely from the increased retail interest in stocks during Covid. Even if the GP got into it by looking at the fundamentals their profit is (mostly) because of its status as a meme stock.

This refrain is common enough, but I don't think it really bears out in the math. Elon just sold $16B worth of stock and the price barely budged. If you've got enough alpha to work with every beta seller out there will hop off and it's well, well before the peak.

> There were plenty of tech losers. You still had to pick the winners.

Yes because I applied basic reasoning. People were still investing in AOL and Yahoo when I picked Google. Seriously. AOL and Yahoo. It was bananas. Every person I knew that had any amount of tech savviness was on Google. The search results were clearly superior. "Invest in products that are better" should be a meme on WSB or something.

What I didn't mention above was that in the mid 2000s I also made money off of oil because I was following China's modernization and politics in the middle east. People back then pushed me on just how much oil would go up and when I said I thought it could triple they looked at me sideways. But it nearly tripled then I sold. I tried to get into lithium through SQM, because I thought electric cars and widespread computing were going to strain supplies, but they didn't. That's when I learned the lesson that over time commodities go down.

> If you actually followed this advice, you'd probably be worse off than investing in the s&p - even if you did pick good stocks.

Not really? Buying in at the very lowest part of 2009 gives a lot of range to play with. This bullrun is much, much longer than most, but over time I think it's easier to dodge the correction than to call the top. The reason for this is that to call the top is to predict when human irrationality reverses. Something I'm not great at doing. What I'm good at is first principles. And at some point I don't care how much blood there is in the streets. That fucking share of Apple is undervalued enough to where I would sell priceless art to buy it.

Also why are you calling his actions naive ? He made money as did others.

To me looking at the stock pricing, Tesla looks like a software company where tremendous growth has been occurring and is expected to continue for some time. To some extent they are a software company, but that software so far has seemed to me to require quite an expensive set of hardware to be sold with it in order to get the software and continuing monthly/yearly/feature revenues sales. This has worked for Apple, so it's not unprecedented, but it'll be interesting to watch how long it can last.

SpaceX makes more sense to me with having high valuations relative to revenues, it's a services company. The service is getting things to space and now also providing internet access. Tesla doesn't look like a software or services company to me, at least not yet. But maybe I'm looking at it wrong?

I'm not currently invested in automotive. Just drive by some dealerships, empty lots. Not because they are selling out but because business is bad. There will be a work from home permanence, the inflation reality will destroy the automotive industry. The only thing keeping them barely afloat is low interest rates.

Then you also have the market disruptor of Tesla. Ford and GM obviously have some fantastic products coming and even some already here. EV silverado and hummer are amazing. Mach-E and EV f150 are possibly the best.

EV cars is a new generation of vehicle and will harm the existing auto industry. Ford and GM are obviously going to survive no problem. They arent worth a trillion $ because they are behind but have significant costs upcoming. GM and Ford's upcoming profitability is going to be quite poor.

Stellantis looks like they are too far behind. Ram revolution silouette looks good but if the Chevy Bolt proves anything... building a good battery has many hurdles. Stellantis has nothing coming soon and may just die.

>To me looking at the stock pricing, Tesla looks like a software company where tremendous growth has been occurring and is expected to continue for some time. To some extent they are a software company, but that software so far has seemed to me to require quite an expensive set of hardware to be sold with it in order to get the software and continuing monthly/yearly/feature revenues sales. This has worked for Apple, so it's not unprecedented, but it'll be interesting to watch how long it can last.

Tesla's first disruption is that after the car leaves the lot. It continues to get better. The traditional auto industry, you leave the lot and your car will be that or worse forever.

The second big disruption is efficiency. AC motors have regen, their motors are ~90% efficient. This creates the new generation of car. A model 3 performance(inexpensive sedan) has a 0-60 of 3.2 seconds. That's faster than all production Corvettes. Faster than a Hellcat. As fast as a Mclaren F1 from back in the day. About as fast as a Nissan GTR or Porsche 911. All the while not being annoying loud, far more practicality, and no emissions.

The most recently disruption... Tesla is now the fastest car with the plaid edition. 0-60 of 2 seconds model s plaid means it's faster than the Demon. Faster than all hyper cars. Yet at significantly cheaper price point. The roadster coming with compressed air to make it faster? Ridiculous.

By the time Ford/GM really get going, Tesla will not have sat around. They will have moved forward.

This is why Tesla has a ridiculous valuation. They effectively are the only competitor in the auto industry for the next several years.

1. You don't have concern yourself with market impact

2. There are niche opportunities that lack the capacity for funds to bother spending their time on.

Institutional portfolios have access to more opportunities and talent than retail investors.

Does it mean that the price is going to go up? Suppose everybody thinks like you (I assume everybody does), the market price may reflect anticipated profits already and doesn't necessarily have to go up.

Also success of Tesla isn't the same thing as success of electric cars.

Trying to time the market is akin to individual stock picking.

When it works, it’s usually just luck.

I keep "beating the market" too though I calculated my risk adjusted return and with that metric I wasn't.

So really I was doing better because I'd cranked up the risk, and fortunately we've been experiencing a bull market.

Hard to say whether I've really been making savvy choices or if it's just been a bull market trend that has been saving my ass.

Exactly. Tell me how you did in 2008, not how you're doing in a bull market.

I think the dogmatic "nobody can beat the markets" is hurting people who then think they may as well give up, and patently not true when you look at traders who beat the market year in and year out, and minimize their losses when they do lose.

If "beat the market" means that you can predict exactly if and when Russia invades Ukraine, then the answer is NO, you cannot know if some drunk soldier is going to accidently shoot off a missile and start a war.

On the other hand, if "beat the market" means that you invest in companies with solid fundamentals and solid management in areas of the economy that are not shrinking at prices that are historically low, then yes you can beat the market in the long term. Buffet and Munger are obvious examples of this.

If "beat the market" means buy everything except NKLA, because that company has obviously been a scam for over a year, then yes "beating the market" is very easy.

Tldr; way too many people believe that a lot of people can beat the market and that is what actually hurts the most investors.

edit: spelling

An important point here is that since nobody knows when this crash will happen or how long it will last or where the bottom will be, you should still keep investing in the companies you think are fundamentally strong and avoid trying to time the downturn.

https://markets.businessinsider.com/news/stocks/big-short-in...

In 1997 a friend who worked at Cisco told me to go all out on Iomega. He also advised me to invest in some 3D storage startup which well went nowhere. No matter how smart you are you just have to play percentages.

Even better consider the case of Cisco itself. It reached market cap of 500B around 2000 and despite being a solid company has not performed too well.

Thus it is quite conceivable that the inevitable market correction will bring the high flyers down.

That is Apple will still be extremely strong, Google might suffer a bit because of dropping ad spend.

Companies such as Shopify, Tesla will actually need to reach reasonable P/E ratios, not the insane ones now.

I don't think that you can expect the stock to be where it is today in 2024 if the PE actually goes down to 12. You'll need to buy it now to lock in that PE of your purchase price.

But it’s not enough to pick winning industries. In every industry there are winners and losers. You have to pick winning industries and winning companies. And sometimes winners become losers. So there’s a timing aspect also.

EVs are going to succeed but I don’t think Tesla was ever a guaranteed success. And Tesla is not guaranteed to keep winning (though they have a great head start and very strong moat).

Maybe everybody knows Tesla is going to win out, therefore everybody wants it, and the price rises like crazy. And then the stock is way overpriced for what you get, and people like you still keep buying it.

There is a reason why Buffet needs to look into the numbers before deciding if something is a good buy or not. You buy underpriced, and sell overpriced. And you just cannot make that judgement without looking at the numbers.

There is another simple theory about your single stocks outperforming the index: smaller cap stocks generally outperform the index. As shown in this video, a monkey can pick stocks and outperform the index just because of this simple reason: https://www.youtube.com/watch?v=5_3Ra-Q6vK4.

> People keep telling me this, but I keep beating the market.

"Humans keep telling me it's hard to predict football games, but if you just squeeze your tentacles up and down enough you will get it right as I did"

-- Paul the Octopus, who predicted all world game results

There are millions of people trying to predict the market. Of course there will be people that did good, and these people (such as yourself) will all be convinced that they got it right for a reason.

But individual experiences mean nothing against the law of large numbers. You yourself have no way to know whether you're good or lucky, unless you show us an algorithm that consistently achieves the results you claim to enjoy.

Remember these simple facts:

- the less you trade, the further away you are from your real average predictive power. If the game is a coin toss and you play 2 times, there is a 25% chance that you get a 100% success rate, and go to HN to boast about how guessing a coin flip is easy. Try to keep that performance after 5000 games and it's an other story.

- Are you able to compute your idiosyncratic returns correctly? Can you show us that your portfolio returns, once residualized on sector, country and beta, are actually any better than a random pick?

- You pretty much only talk about good old common sense fundamental quality / value, which is far from being a major part of equity returns. You reasoning will work for one stock, and not for an other one. A sime value based strategy as you describe is vastly negative on a 20 year period - in absolute terms (not even compared to the market).

- You seem to have no understanding of diversification, and idiosyncratic risk. Companies can fail for an infinite amount of reasons. The less positions you have, the more sensible to "single company failure risk" you are exposed to. Very good companies, with solid earning and projections, did fail on the past, for reasons such as "top management scandal", "defective line of product", "banned from operations in a country", etc etc.

To anyone reading this comment, just remember that 90% of stocks returns do NOT come from the company itself. It comes from the drive of the market or sector as a whole. By investing in broad index funds you lower your specific risk, and get overall exposure to what drives the vast majority of the stock returns.

Would note that we’ve been in about a single interest rate regime for almost precisely that amount of time.

Almost none of the posts talk about what investing traditionally has been for-- buying future cash flows at a current discount. Sign of the times....

This doesn't sound right. I'd put them as way above average. Possibly leading the pack out of the public companies.

Because even bad stocks are an essential component of a balanced portfolio if they reduce overall portfolio beta (volatility).

The name of the game isn't pure gains, because the gains are not guaranteed. You want to make gains and hold onto them.

And no, you don't know for sure that Tesla will eat their lunch. You have a very high level of confidence that they will. So does the rest of the market, that's why Tesla is trading at a huge premium relative to its financial fundamentals. But this wasn't always the case, and there were more than a few times when Elon Musk brought Tesla to the brink of bankruptcy. If you were confident that Tesla was going to pull through, even back then, you either a) knew something the market didn't, b) were mistaken/wrong (but luck pulled through for you in the end), or c) you were reckless / irrational.

And they still have terrible quality of assembly.

"Telsa, Apple, Shopify, Amazon, Google."

Isn't this really just 'invest in SV scaleups? What are the forecasts for Xiaomi, or s Panasonic?

You can make money on things that go down as long as they are not too strongly correlated with other things, and you maintain a constant fraction portfolio. One of the search terms here is "volatility pumping", I believe.

Commodities are a stabilizer for portfolios… they let you take more risk in other parts of your portfolio because they are easily marketable, non-productive assets.

Equities on the other hand have unknown amounts and timing for cash flows. Hence people bid the value of stocks up, down, and all around.

And this is why I am going against the advice of the majority(?) and trying to time buying into the S&P 500. I am looking for another crash like the one around when COVID started. Am I wrong and should I also not try to time the market?

Another is this: What if the market crashes 40% but then goes back up? Do you buy at 40% down? What about 30% then?

It's easy to say "well I'll just buy at the bottom" but you can't know when the bottom is until well after it's happened.

The other major piece of the puzzle is that during a 30-50% crash, everyone you know and all the media will be screaming in your ears about how everyone is losing all their money in stocks, and that the only reasonable thing to do is sell now so you don't lose it all. Do you have the stomach to put all your money into the market in those conditions?

If I was 70 and couldn't afford a 5 year correction, things would be different

furthermore, Musk is very impulsive and could already have been cancelled by the SEC for his mistakes: I bring that up to point out that by hitching your wagon to this one individual (or Henry Ford) you are taking on enormous risk, risk that is diversifiable and there's no reward for.

However, I am sure there are many people who have lost money (or made much less) with reasonings that may be at least as sound as this one.

Throw in an investment in Apple when everyone started switching to Mac circa 2006 (I told everyone who would listen to buy it, but I was a college freshman, so no one listened, but it was so obvious), and you got a stew going.

It didn’t take anything fancy to crush the market if you started 20 years ago and were dialed into tech.

Remember, you don't have to beat those super smart well resourced AAA-grade investors. You just have to beat the average schmuck with some skin in the game.

- Buy S&P ETFs, most preferably by Vanguard, because they are a non-profit and thus have very low fees

- If you have a large sum of cash, go all-in immediately, don't wait for the perfect time

- Now, just wait, ideally 10+ years, before looking into your account again

Vanguard is certainly a for-profit organization [0]. What, I think you wanted to say, that many of the Vanguard funds are index funds that do not have exuberant management fees.

“The Vanguard Group is truly a mutual mutual fund company. It is owned jointly by the funds it oversees and thus indirectly by the shareholders in those funds. Most other mutual funds are operated by management companies that may be owned by one person, by a private group of individuals, or by public investors. ... The management fees charged by these companies include a profit component over and above the companies’ cost of providing services. By contrast, Vanguard provides services to its member funds on an at-cost basis, with no profit component, which helps to keep the funds’ expenses low.”

https://www.inquirer.com/columnists/john-bogle-vanguard-scra...

That might not be the best idea because of escheat. Here's a story about someone who didn't check on their stocks for years and the state claimed them. https://www.npr.org/transcripts/799345159

- ETFs, Vanguard is a good choice for most. If you're older and might need a large percentage of the money fairly soon, consider getting some bonds as well.

- Don't try to time the market

- Don't think you're smart

The only personal difference is I prefer FTSE All World as it is diversified into over 4000 global stocks, while the S&P 500 is (obviously) 500 American stocks. That being said the S&P 500 has been outperforming the FTSE All World for a long time, and I certainly don't want to give anyone specific investment advice.

Additionally, because of many societal conditions, right now many people think they need to hit on a moonshot to have a good life. And given the direction that inflation and many other things seem to be headed, it's harder to argue that they're wrong. Slightly increasing your financial floor matters little if the floor is still dirt.

That said, most of current CPI "inflation" is not economy wide price increases, but comes from 1) car prices, because car manufacturers massively messed up and production is way down for the past two years, and 2) energy, which is from several global market issues. There's also housing, which is not in CPI, but that's also easily attributable to underproduction of housing since 2008 (and probably even for decades before that, honesty).

We are actually in incredibly good economic times, especially considering the massive destruction that the pandemic has wrought, and in the US, the lowered number of workers due to years of reducing immigration. I am glad people are not overly exuberant, but I with they were focused on the things that mattered more.

See for example: https://ritholtz.com/2019/08/death-of-equities-40th-annivers...

Nitpicking but S&P has multiple indexes. And you probably mean just a total stock market indexes; not necessary S&P.

Buying an index fund full of stocks at their current market price is no more illogical than running code you didn't write yourself. It's way way less work, it probably works better.

Better yet, trusting someone else's market price is much easier than trusting someone else's code because of the thousands of black-hat investors searching for profitable vulnerabilities in the market prices.

This x1000 I've seen plenty of friends of friends who probably had issues passing HS Algebra thinking they're "Daytraders" because they made some money off BTC or GME in the past few years and I just cringe so hard. My index funds consistently return ~20% a year lately. If you aren't even matching that you aren't a trader you're a sucker.

Kind of. What you have to remember is what game you’re playing. While financial firms can outspend and out-research you at an individual level, they can’t take the same risks you can or move as quickly as you can. If I decide I want to go all-in on some company I can just do that. Your friendly neighborhood hedge fund? Not so much.

Most people should buy index funds or similar, no change there, and even those who decide they want to pick stocks should mostly have a broad portfolio, but you can pick stocks if you want and you can be successful.

If you put all your money in at thr wrong moment, like say the Nasdaq in 99 then you waited 13 years just to break even.

But if you bought monthly you would have done very well because you averaged into the market.

The alternative is if you really understand valuations, diversification, risk and market psychology, like I do, then you can consistently beat the market. Most people cannot and most people you pay fees to do it on your behalf won't.

You could consider buying berkshire hathaway instead of a stock market index.... assuming the lead investors don't die too soon.

There is also a catch: Suppose someone reads this, thinks "I think I could be as good as it as this HN user" understanding valuations and market psychology and whatnot.

Maybe you can. I am not sure if I can. But one thing I learned while trying, studying some companies and trying to find out where I could have relevant domain insight and then somehow coming up with an estimate for correct stock price when to buy/sell is a hugely time consuming hobby which isn't super fun.

I’d need to do a Monte Carlo to provide hard evidence but I’m fairly sure that lump sum investing is, on average, going to provide the greatest return. For people just starting out in investment, whose appetite for risk is high, that seems the way to go.

Edit: Leggio and Lien (2001):

> We find DCA [dollar-cost averaging] consistently remains an inferior investing strategy to Lump Sum investing using the risk-adjusted performance measures.

> The failure of DCA as an optimal investing strategy for all assets and portfolios considered is likely because DCA is a conservative investing strategy best suited for investors interested in a forced savings plan that avoids the consumption of earnings.

I invest monthly because I get paid monthly.

I invest lump sums when I get windfalls, like bonuses, likely because I haven't invested as much as I want because my repayment mortgage (saving me 2-3%/annum) eats all my monthly income.

I sell everything when I need to buy a property because I'm not rich enough to use my stocks as collateral.

I think it's more than that. There are people with more capital etc. who specifically use that to take advantage of people like you. I don't just mean pump-and-dump kinds of stuff either. HFT exists to take advantage of the arbitrage opportunities created by traditional kinds of trading in aggregate (and sometimes to take advantage of other HFT bots) creating a kind of "friction" that is hard for less capitalized traders to overcome. The market is as much of a fight as a race, and it's really hard to win against the heavyweights unless you're one yourself.

> Picking individual investments is mostly a sucker's game.

Definitely true in the short term, for the reasons mentioned above. Still mostly true in the longer term. At least there's a chance that a sufficiently canny investor can pick a basket of stocks that will grow over time, but statistically it's almost certain that you'll fall behind the S&P index. Even the very best fund managers, with all of the resources at their disposal, rarely beat that more than a couple of years in a row.

That right there is the best advice. If you want to get rich quick, you're going to have to make some calculated bets with higher return and thus higher risk. However, if those bets work out and you do become rich, don't fool yourself into thinking you're some kind of super genius that can consistently beat the market.

This can be a hard lesson for people to learn (it took me a long time), because in most aspects of life success is more skill based. With investing, there is more decoupling between action and outcome due to randomness, and you have to always consider you may have made the right choice and lost, or you may have made the wrong choice and won. In the case of the latter, take your winnings and be happy, but don't delude yourself into thinking you made a good play. This is extremely hard, you have to be willing to put your ego aside and realize you actually made a mistake that made you a lot of money.

I think ordinary people with the right knowledge and foresight at the right time can beat the market in the short term. The trick is to be extremely patient until you have a reasonable level of confidence you have an edge in a bet with an asymmetrical return, and then take a position with conviction. I've done this a few times in my life, and the knowledge, timing, and luck all happened to work out for me. I've also had that feeling a few other times where things went south. Luckily for me the winners far exceeded the losers. However, I wouldn't con myself into believing I can consistently generate an edge. I simply made a small number of calculated bets when the stars all aligned for me. It's very possible the stars will never align for me again like that, which is why I've now moved most of my money into ETFs and other safe investments.

One way to spot someone who doesn't know what they're doing with investing and trading, is you never hear about their losses. You never hear about their net gains. You never hear them tell you the story of when they drunkenly made a really stupid leveraged stock pick that just happened to work out from pure luck. No, you hear all about the winners, all about how they knew for sure it would work out for all these reasons. You just see the overflowing ego that gambling has drummed up, rather than the intellectual honestly of someone who has sat back and grappled with the tough question, "did I make all this money because I'm smart, or am I just a dump and lucky ape?"

Don't fool yourself into that, but as the Kelly criterion advises, do play harder with house money.

An expert in some particular field sees different opportunities and make strong educated guesses vs a trader who will react on financial metrics.

lmao god this feels so much like the mindset of so many tech people in general. They were right about one thing so naturally they're of course right about this next thing...

>Taking on risk over the last few decades has paid off in spades.

There's two types of risk here: risk that is compensated by higher returns (eg. buying stocks rather than bonds) and risk that isn't compensated by higher returns (eg. buying OTM options rather than stocks). It's not really clear that higher than expected returns in the past decade or so for "tech stocks and/or crypto", mean that they have higher risk-adjusted returns in the next decade.

This can be observed in certain illiquid markets, e.g. for a specific bond of a company. In those cases, the "last trade price" is meaningless and it's very important to instead look at the bids and asks in the order book.

The best measure if pricing in my view is "what average price would I get or slippage would I see if I sold X shares right now?"

The lack of "crossing" between those two doesn't mean no one is willing to trade.

(edit: inserting disclaimer "serious question" lest i get downvoted)

I do think the "correct price" is near the middle of the spread though. Because this sort of thing happens not just because of illiquidity, but also because everyone involved knows what the "correct" price is. (E.g. because bonds have very predictable cash flows.) There's no difference in opinion large enough to convince a trader to cross the spread.

The good coming out of this is the visibility of how strongly dependant cryptocoins are.

Ukraine kicking off is not going to help in a sane world, but it's not a sane world so I half expect all time highs while Odessa burns

I guess a few facts like markets are not always efficient, they are often irrational, there has never really been a "free market", its been distorted by governments and powerful agents... Corporations were the ones who created market regulation so that they wouldn't be subject to its vagaries.

One small inaccuracy is the claim that there is only one place for each stock. That has not been true for many years. In the US that was changed by https://en.wikipedia.org/wiki/Regulation_NMS . NASDAQ is the primary listing exchange for MSFT, which means they will hold the opening and closing auctions, but it can be traded on any equities exchange, NYSE, IEX, BATS, EDGE-A, EDGE-X, you name it. RegNMS also has rules that if there is a better price at another exchange, the order must be routed there. This establishes the "NBBO" - National Best Bid and Offer, so in a way there is always one best bid and one best ask, but it's an aggregate over all the exchanges.

But US markets have some special Reg-NMS rules that glue together things across exchanges. Being from Europe I'm not so familiar with it, but I understand it causes some interesting games to be played.

If you want to actually understand how the market works, there's a fair bit more reading to do.

"A single market to trade. All stocks for Microsoft (MSFT), are traded on the NASDAQ exchange. All stocks for Ford (F) are on the NYSE."

MSFT and F both traded on 16 difference stock exchanges, not to mention countless "dark pools", each with their own book of bids and offers. But there's a national best bid-offer (NBBO) that all exchanges must respect, so it can behave like a single market. That's what Reg-NMS is about. The benefits of having several exchanges competing each other, while trying to retain the benefits of single market. This is also where HFT enters the picture with latency arbitrage and other trading strategies when prices on those markets get out of sync.

20 years ago, you could say that MSFT only trades on NASDAQ, but that hasn't been true since Reg NMS came into effect in 2005. Each stock has a primary listing market that controls things like halts and opening/closing auctions, but the stock can be traded on any exchange, each with its own dynamics.

> What you can buy it for? (Your best bid)

> What you can sell it for? (What you’d ask for it)

They have it the wrong was around I think in that the amount you can buy an iphone for as a taker / customer is generally higher than what you can sell it for so what you can buy it for is the (dealers) ask price and what you can sell it for is their bid. If you are a dealer / maker with a stack of iphones sitting there then the higher price you offer to sell them for is what you ask and the bid is what you'll offer for people selling you their phones.

There are some other simplifications too like "All prices are completely transparent." In an ideal world but in reality there are off market transactions, wash trading, faking and so on.

In most scenario (assuming good demand for the stock you are buying and a functional market etc.,) a market maker, looking at their order book, buys 7 items from A. They sit on it until they are able to dispose off them to a buyer. In effect, you, as a buyer is buying a stock from market maker.

Most of the equity market is not P2P but mediated by market maker. They take the liquidity risk (i.e., holding a bad stock if demand plummets) and are rewarded for that by making money off of every transaction through bid-ask spread.

Of course I'm greatly simplifying as an equity order goes through a bunch of intermediaries but Market Maker play a central role here.

What this means is that the shares eligible to transact do so immediately, and the remaining shares sit on the order book and wait for someone to be willing to trade at that price.

There is a specific option that you can set (usually called "all or none") that will prohibit partially filling an order and only allow it to execute in entirety.

"What makes us Tick" was a high-quality cartoon that explained the theory of the stock market, and the benefits of captitalism in general. Of course, its a Cold War era propaganda cartoon, but its still a really clear and simple explanation.

The "Ticker Tape" may sound quaint, but "Market Makers" are really just those round-lot dealers that are discussed in the cartoon. The overall explanation remains valid for today's market, just with more automation / computers involved today rather than humans on a telephone.

In particular, I'm really curious about ETFs/mutual funds and what exactly happens "behind the scenes" when I buy a share i.e. what a share of a fund represents, how it translates to individual companies' shares, NAV, creation/redemption etc. I've heard these terms before, but I haven't been able to build a full picture.

If you're trading indirectly, which is not unusual with a brokerage, you should be aware of what is meant by "best execution", and I offer this article with an explanation in FX: https://medium.com/bull-market/oranges-and-lemons-the-fx-sca...

The case where the bid is higher or equal to the ask is known as a "crossed book". I most cases, this should never happen and if it does it would be as a result of a bug in the matching algorithm. If you place a buy/sell order with a price that is in excess of the best ask/bid respectively then that order will be matched against the opposite side. Under normal conditions what you suggested should be impossible.

If you want to know more about how order books work, I wrote an article specifically about how this works mechanically: https://www.machow.ski/posts/2021-07-18-introduction-to-limi...

Generally if a bid is introduced that is higher than the ask, the volume at the ask is matched, then the volume leftover at each ask level is matched in order of price (then time).

First case: you ask for 100 and then I bid 105 --> transaction clears at 100, the ask price

Second case: I bid 105 and then you ask for 100 --> transaction clears at 105, the bid price

This is because I implicitly think about bid offers as "I want to buy this for at most X dollars" and ask offers as "I want to sell this for at least X dollars".

I might be completely wrong though.

I would also look at long-term history, business cycle (in the stock market terms), inflation and rates, liquidity crises as a background for investing. Those are much more valuable for an investor than order book details. My 2c.

However, this isn’t as great as it sounds. While the European model for healthcare and education is better, their pension schemes are arguably a much worse deal than what Americans can have.

In Europe, you’re basically paying the government to take your money and invest it in much too conservative, in fact, negative-yielding! bonds right now due to pension fund mandates.

You can’t take the proper amount of risk given your age (in your 20s-40s you should be almost fully allocated to stocks) because the pension fund needs to constantly be paying out money to old people—they can’t risk huge drawdowns.

There’s a surprisingly large amount of middle class Americans who will retire millionaires just because they are able to save for their pension privately and take the proper amount of risk for their age (eg. Target date funds).

Meanwhile, in Europe, governments shelter people from the harsh realities of how financial markets work, but you have to hope and pray that enough people are born in the coming decades to make up for the conservative pension mandates. And you have to pray that the government allows you to retire sometime before you die (in the nordics, retirement ages are constantly being pushed back and pension benefits are shrinking...due to said demographics).

I predict every country will eventually move to a hybrid private/public pension model like the US over the next 40 years. So you'll have to start caring eventually.

I'm not sure pensions exist in the US beyond a few public sector ones. The US model is entirely private at this point for all intents and purposes.

Also keep in mind that only about 55% of the US population owns any stock (including retirement accounts) [0], so (IMO, not an economist) the US is most likely looking at a retirement crisis in the coming decades.

[0] https://news.gallup.com/poll/266807/percentage-americans-own...

This is intended to be supplemented with private investments via 401k & IRAs, which are actually relatively new programs (created in the late-1970s, but nobody even talked much about them until the 90s).

So while most millennials understand they need to be saving privately in these vehicles (r/personalfinance has 15 million members), there's a huge forgotten generation in the middle who slipped through the cracks between the transition from industrial-era corporate pensions to personal saving.

These are the folks who will unfortunately bear the brunt of the retirement crisis, having to get by only on Social security.

This is a myth. People struggle on state pensions throughout Europe, but for some reason young Americans idealize everything that comes out of Europe.

In Germany(a country of 80 mil), the average pension is $1000 once you get to 65. In France it's not much more. The social security in the US beats that, plus you can usually afford a private pension, because the government doesn't take 50% of your paychecks.

I personally know someone in Austria that worked all his life for the railroad, then he got sicker and sicker, but the state wouldn't give him a disability pension. He could barely work sitting all day. Then he got disability at around age 60, but he needed money so much that he had to collect scrap metal to make ends meet. Very sick, after 60 years old, collecting metal. This is just an anecdote...I know, but still.

In France, the average pension is 1393€ (~ $1574) [1]

Also the retirees purchasing power is higher than the working population [2]

Don't get me wrong, there are still too many retirees with too little money in France. But on average, the retirees are doing OK compared to the rest of the population.

[1] https://cleerly.fr/retraite/retraite-moyenne

[2] https://www.lefigaro.fr/retraite/les-retraites-ont-un-niveau...

This seems like a serious bug in the system, doesn't it? Why would old people retire as millionaries while young people struggle working long hours and can barely save anything?

The fact that young people struggle really doesn't have much to do with this.

The problem is that housing costs rise to suck every spare penny of income from pretty much everyone so very few people have spare money to put into those isas.

European governments see the demographic timebomb coming, so they massively incentivize their citizens to invest in a primary residence, treating it as forced savings. This inflates local real estate values to ridiculous levels, especially while interest rates are low.

However, incentivizing your citizens to take leveraged bets (big mortgages) on a single piece of real estate is...not great.

This means the investment portfolio of the average European citizen is ONE specific apartment (zero diversification), and negative yielding sovereign bonds (via government pension funds).

Since most European mortgages are not fixed rate, it will be interesting to see what happens as interest rates start rising in Europe.

While the bonds will start paying better interest, that mortgage exposure might start to wreak havoc on the average citizens finances...

You can be in the top 1% by income in London and still simply not be able to afford a small family home.

Home equity wealth inequality in crippling.

Nor can we assume that the exceptional stock market returns of the past 15 years will be repeated, which means we need to save more for the same result.

I feel great pressure to earn a high wage in order to save a lot of it into a pension. This feel like a matter of survival.

This was of course obvious already a while back, so the government decided to introduce additional ways to encourage saving for retirement (by giving tax discounts). However, they also managed to screw this up, because only contracts from certain insurance companies apply for these tax discounts. And these contracts have such a high management fee, that the real return of those constructs is negative.

Yet there's a surprisingly large amount of middle class Americans who have no retirement savings; either due to YOLO, or medical emergencies, or misunderstanding how to invest towards retirements.

I would love to see some data around this. Because what I keep hearing (being in India) from the usual suspect sources is mostly gloom and doom[1]

Additionally, only about 1% of those millionaires are under 35. (This is a point that gets lost in the debate about inequality, in my view; most wealthy people are old for what I think are extremely obvious reasons.)

https://spendmenot.com/blog/what-percentage-of-americans-are...

In the UK almost everyone will have been moved over to a "defined contribution" pension whose value is determined by the stock market, usually in the form of a "stakeholder pension".

I don't "do" the stock market but I do have such a pension. And every few months sweep spare cash out of my current account into an index fund. Effectively I pay people to worry about this stuff on my behalf.

People who retired more than about 10 years ago are far more likely to have "defined benefit" pensions whose value is independent of the stock market.

For most people outside the very niche finance and tech investment bubbles stocks are largely understood as a form of gambling and managed funds as a high yield alternative to a savings account with a small risk of losing money (but this requires some disposable income so again this is somewhat self-selecting).

The ordinary Hans Wurst (German Joe Blow) just follows the economy section of the news for a general feeling of if things are going good or bad because line goes down means prices go up and they probably won't get a raise.

Shares (and all their financial derivatives) are a good hedge for profitable limited companies, because they either go up in value (yay! profit!) or down in value (yay! tax deductable loss rolled over to next year!). So long as the company is otherwise making a profit, shares are actually pretty hard to lose out on.

Also pensions. Most pensions are backed by index funds which are generally related somehow to stocks and shares. If you need to manage a pension fund, you have to pay at least vague attention to the stock market.

I once worked at a company which used a money market fund for its cash. That gave them a slightly better return than a bank account. In the end, not sufficiently better to be worth bothering with.

You can get whatever risk profile you want from the stock market in return for less yield. If you can accept two-nines certainty that you won't lose half your money in six months, any broad index fund will do. That would be acceptable for a lot of "modest businesses" which find themselves with "6-7 figures cash reserves". If you need better, you can do fancy things with options, or put a fraction of the money in the bank and invest the rest.

(I am a financial professional, but not in this field, and this is not financial advice)

The US stock market has been ridiculously pumped from the last decade-plus of money printing, I wonder how many people think that's normal.

So if your business is doing well you can avoid putting all your eggs in one basket by investing some cash personally outside the business. And the easiest way is to jus put it into an index fund and then concentrate on your business.

By all means plow a lot of it back into the business, but there’s good reason to pull some out over time as well.

Instead, invest a regular amount of money monthly into ETFs. Those are relatively low-risk, but should still yield significant returns over the course of decades.

It's true that most people (at least in Germany) don't trust the stock market. The problem is that your wealth is being eaten up by inflation and interests on savings are low or even negative. You will lose money. In addition, Germany's mandatory pension funds are in a bad shape and most private insurances (e.g. Riester) are not worth it.

The situation is not the same as in my parents' generation and unfortunately, a lot of people are not realising that.

In Switzerland, I have to pay ~0.1% stamp duty on every purchase and sale of stocks and ETFs (in a Swiss broker). The UK has a 0.5% stamp duty on stocks. The idea for these brokers to compete on price doesn't make much sense at that point. It's "fine" that the normal fund has a 0.5-1% fee. There's some movement here, but only if you care to engage outside your existing bank (IBKR in the UK, Avanza++ in Scandinavia, Degiro in Europe in general).

Investing is good, and---as has been said---pensions are often invested in the stock market, whether you know it or not. But you just don't talk about it, because being active is costly. In Sweden, the defined contributions are auto-invested in a balanced fund unless you engage. There's something to be said about having sane defaults when you create a system.

As for the US, I'm not sure Robinhood was a step in the right direction. We should encourage people to own companies, not try to profit from Brownian motion. But that's perhaps a topic for another discussion.

Finally, I'm heavily into the stock market. I have several accounts across the world (though not really by design). I'm fascinated about this oddity that I can buy more food in the future just by having a different piece of paper, compared to someone else. But I also spend a stupid amount of time trying to find ways to reduce cost of investments. My guess is that most people don't, and it's kind-of the first step for a European that's paying >1% in fund fees. Or who don't even know how much they're paying.

Some would say this is typical behaviour before a crash. Business people become folk heroes (Musk) and the news is all about stocks and macroeconomics.

When the media started pushing GME, people went and bought GME. When the media started pushing btc, people went and bought btc.

Stocks aren't being encouraged, therefore most people don't do it and instead cluelessly dismiss it mostly as gambling. Same goes for cryptos.

Right until the media pushes it, people buy into it, rich people sell causing prices to crash, and the cycle of cluelessness repeats.

Sometimes you're forced to (when an investment is tied into a basic necessity, like a house), but you're always going to be at a disadvantage.

> investment is tied into a basic necessity, like a house

? What does this refer to?

Fact is, as soon as you've got a meaningful amount of wealth, you're going to want to invest it so you can either get income from it or grow the principal. It could be in a home, multiple properties, or the stock market.

> People I have known in the past (old people) didn't do stock market either. They all seem to have lived a normal life (decent jobs, decent house, decent family). Nothing extravagant but they got enough money to be "happy" in life.

No offense but you're going to have a tough time comparing to a boomer in terms of wealth generation and building if you're a millenial. I know people who got houses handed to them for very cheap 30-40 years ago, and those houses are worth tremendous amounts of money now. On top of that they have good pensions and insurance from a long time ago. Or they have a rental contract where they're paying 1/3rd of their neighbors so their expenses are low.

There's a great income and wealth divide in Europe between the haves and the have nots, and the haves are very good at keeping their wealth and passing it down to their heirs. Meanwhile in most European countries, punitive taxation makes it extremely difficult to move up in social class, even from middle class to upper middle class.

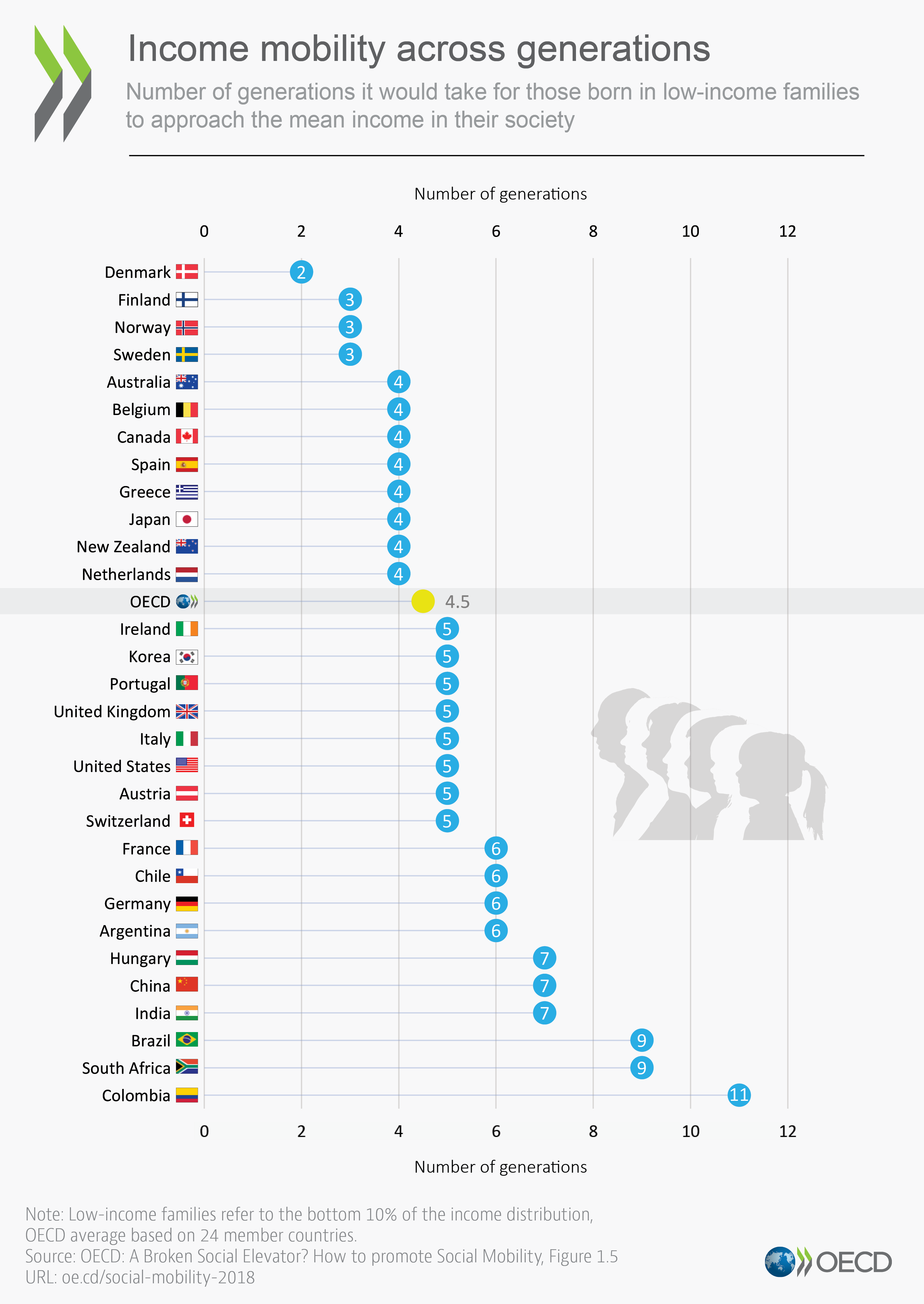

This is not true. Several of the highest taxed countries in Europe also have the best social mobility in the OECD: https://www.oecd.org/els/soc/1-5%20generations.png

It might be the case that Germany is particularly rigid, but that is not transferable to most of Europe and certainly can't be attributed to taxes.

Low inheritance taxes are actually a great predictor for maintaining social inequality over generations. If you wanted to reduce social inequality you'd instead want to drastically lower VAT (which disproportionately affects poorer people), adjust income taxes to lower the tax burden on lower incomes and raise it on higher incomes, and drastically raise taxes on income from capital (rather than labor). This isn't even simply an opinion, this is scientific consensus.

Do you have one for mean income to upper class by chance? Even +1 Std Deviation move would be significant in terms of wealth building.

Maybe less so in the USA? Not sure.

But a lot of computer folks have spare money at the moment, and in that situation you have a few options: consume more, keep it in a savings account, or invest. And some significant proportion choose invest.

Keep it in a savings account is a common option, but quite a bad idea.

Probably the majority of people who invest do so in property, considering it safer than stocks (which I disagree with, although there are other reasons to like property).

This may be changing a bit in recent years, because access is easier now. In Sydney I see adverts for stock brokers at the bus station.

Seems like some gamblers have switched to the stock market to get their fix too.

It could also be that you prioritize investing money into a house instead?

Stocks are considered "risky", but if you have a 10+ years timeframe, an index fund is not risky at all.

I also have 75% of acquaintances that don't do stock market or crypto. And that's the reason why my savings are outperforming all of them.

In the US, the majority of adults are invested in the markets (https://news.gallup.com/poll/266807/percentage-americans-own...), whereas in Europe the number of people invested has historically been lower (https://www.ft.com/content/31c4d453-498e-4cc2-b14f-d7e8b17b9...).

This makes sense when you think about it - in the past you would have built habits and understanding from relatives and your community (e.g. "Don't invest in stocks that's gambling and they always crash!"), whereas since the Internet came along people have more access to data and perspectives from more places.

All of the above said, the last few years, and especially since the lockdowns, the behaviour in the markets has been really alarming. The FT.com link above touches on this, but the rush into [stocks/cryptocurrencies/leveraged funds/options] is something I've never seen before in my lifetime. I don't think the world has ever seen anything like this level of amplified speculation. Bitcoin, Leveraged ETFs, and Options didn't exist in the 1920's. The Netherlands had futures contracts towards the end of Tulipmania, but I haven't seen anything to say that they were leveraged.

In the late 1990's it was clear and readily apparent to everyone that the Internet was a massively important step forward. We agreed on that. It wasn't a controversial or widely disputed viewpoint. The market still imploded because of the sheer amount of rampant speculation, so to think something worse won't happen to a multi-trillion dollar market based on a technology many people think only has value for running Ponzi schemes seems to be pretty irrational.

To top it off, the wall of hype seems impenetrable at this stage ("have fun staying poor!" etc), so it remains to be seen what happens when the plates stop spinning this time.

tldr; Your grandparents might be proven right after all.

In the 1990s it wasn't clear to everyone that the internet was a massively important step forward. You were younger and probably part of the technically-savvy, forward-looking generation that could clearly see the internet being massively important in future. However, *many* people in the older demographic lacked this insight and didn't fully embrace the internet until the mid to late 2000's. I think we'll see the same thing play out with crypto. Writing everything off in the sector as being ponzi is especially flippant.

Every dollar you get but didn’t work for was a dollar that somebody else worked for but didn’t get. The stock market is full of transactions which yields profits for the rich while leaving workers at a loss by means of lower benefits. I refuse to participate and become a class traitor.

I’ve never worked in an industry which tries to push stocks onto you as much as software development. They keep paying me out options, giving me stock plans, etc. My strategy is to get sell as soon as I’m able, and transfer the money to a savings account in my local credit union. Don’t let them get away with not giving me my money, but don’t let them dictate how I keep my savings.

There is loads of counterexamples for this though. Especially in older countries in Europe it can become very apparent.

Also having wealth (trough inheritance) enables one both more opportunities and reduces risk. A poor person taking a "gamble" on a business (if they can start one that doesn't require long rampup or capital) will struggle to feed themselves if it fails. A rich person (if not just focused on inherited assets) can try multiple times and is often encouraged to because of this but also trough exposure to fundamentals from family.

Off-topic from the thrust of this conversation, but I always considered the above extremally risky. If your company goes tits-up, you loose your job and your savings.

This happened to a lot of people during the dot-com crash of 2000. (Unless you have a high risk tolerance, you will want to diversify much more.)

Employment is by definition exploitative because a capitalist system requires the owner to derive profits from labor, i.e. pay workers only a part of the value they generate. This isn't a value judgment, this is a matter of definitions: the capitalist mode of production is by definition exploitative because avoiding exploitation would steer the owner towards bankruptcy and thus kill the entire business.

The only solution to avoid this contradiction is to not have a separation between ownership and work, to abolish the capitalist class, i.e. ownership of a business is granted by working for that business, with all the rights and responsibilities ownership implies. However the ultimate ideological goal is usually (similar to how Free Software doesn't want to control copyright but abolish ownership of software) to abolish the notion of ownership or even businesses as distinct entities, much like discrete ownership of land was a nonsensical concept before enclosure (i.e. it was "your land" because you used it and the community was okay with you using it).

I think the most frequent misunderstanding of communism comes from trying to fabricate communist structures within capitalist power dynamics. Most of the prominent "communist experiments" had very little to do with actual communism because they were built around the assumption that they were building a foundation for communism to happen later rather than directly building communism in the here and now (hence the Eastern Bloc phrase "real socialism" as a euphemism for authoritarian governments with mandatory labor and limited democratic instruments, none of which is compatible with the definition of communism).

The thing most people seem to forget is that the goal of "abolishing the capitalist class" is to also abolish the working class as a subjugated dependent group because it is only a meaningful concept when contrasted with an owning class. The Soviet Union failed terribly at this by replacing the capitalist class with bureaucrats, effectively still maintaining a distinct working class and hoping he bureaucracy would magically "wither away" eventually while doing nothing to make that happen. They also tend to forget that the distinction between capitalist and worker is purely about ownership and there are many overlapping hierarchies of power, and owner vs worker is merely one of them (although one of the most important ones).

Of course owning these stocks gives me nothing over their monitory value, so having them benefits me nothing over having an interest account with equal interest rate. So I just look at them as a bonus pay with additional headaches (moving money out of the stock market is harder then to cash in a normal check). And as while the power imbalance exists between workers and bosses, I would rather just get paid in regular salaries without the extra complexities.

At most these people do stocks like a person who returns their compost to the city does public gardening.

One thing the article doesn't mention is why people buy and sell stocks. The stock market used to be for companies to raise funds before they turned a profit. Usually for businesses like railways which need huge amounts of capital before they can even begin to operate. Nowadays it's usually companies that are already profitable. Speculation is also a much bigger concern for people than it probably should be. It used to be that just owning a share in a company was good because a company is (hopefully) productive and pays you a dividend. Now people only seem to think about "beating the market" which is a shame, I think.

They also allow liquidity. A public company can't stop you from selling your stake, or buying more. This is something you'd definitely value if you've ever been screwed out of equity at a startup.

Thanks for submitting this (and writing it, author!).

Is he writing for pre-teens?

Suppose there is some difference between buying price range and selling price range. The dealer (middle man) could become temporary in-between buyer or seller and take some of the profit due to this price difference.

For example this could happen at a stockbroker or at a crypto exchange.

Is this behavior regulated, and if so, how?

Crypto is not regulated, so the order book could be completely fictional and there would be no recourse.

If so, crypto exchanges such as Coinbase could make a lot of money this way.

Buyer tells the trader to buy for (up to) 140. Seller wants to sell for (at least) 120. Trader gives 120 to seller, gets 140 from buyer, gets to keep 20 for himself.

If there is no buyer yet and a trader suspect there might be in the future, it could try to buy at 120 and hope to sell in the future at 140. Of course the the sale might not materialize and they will need to take the risk.

Also this is theoretically, the point of High Frequency Trading...

Sadly this is only theoretical, seemly they are quite willing to make the market messy to force this difference to exist so they can profit more, and not many governments so far are bothered by that.

The reason that this trading style is called "High Frequency" is that everyone knows these relationships and therefore it's a race to get there first. Much like the scene from "Glengary Glen Ross", the first person who gets there gets a lot, the second person gets a nibble and the third person gets nothing.

The whole value of this is profits for the firm and high liquidity for everyone else. Not saying it's a noble pursuit, but we follow all the SEC, FINRA and other market regs (most importantly NBBO).

But that is not what I was talking about even. I am talking about the firms that do spoofing, layering, etc...

Basically a lot of HFTs that instead of just doing "daytrading" style trades or arbitrage, attempt to influence the market in some way, hopefully making the spreads bigger and whatnot.

Don't hunt for rising stocks, but chase the falling stocks. Everything that goes down either eventually goes up again, or dies.

While this sounds like it's not helpful, all that's required is figuring out if a company is likely going to die. Even without any manual research, time is ultimately telling. The longer a company at the bottom doesn't die, the more likely it's going to rebound eventually.

https://en.wikipedia.org/wiki/Andr%C3%A9_Kostolany

PS: Don't gamble your life away.

Well, yes, that might have informed his lessons from trading. There's another saying in the opposite direction, "never try to catch a falling knife". https://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp1545.pdf

But it's not an unreasonable approach. Declines are often driven by panic. If you can determine that it's an irrational panic and the fundamentals of the business remain strong, then you can invest while it's undervalued. It's certainly better than buying just after something has gone _up_.

I assume you have good intentions, but your post is severely lacking. One crucial thing with this strategy is time. WHEN is the time to buy a falling stock? While it is falling? Or when it is rasing again? Are we talking intraday or months?

On a long enough time frame, every company will go extinct and every stock will go to zero.

And your post is in direct contradiction of two other common stock insights:

- Don’t catch a falling knife

- The market is efficient. If a stock price goes down, there is probably a reason for it.

The reality is that it's much more complicated than any one liner, and that most normal people that invest, invest based on gut feeling. It only really works by chance. Or they invest in index or mutual funds.

> Everything that goes down either eventually goes up again, or dies.

Sounds smart, says nothing at all. Hence, "buying a beat-down company" is probably not advice that really works. And there are so many companies that never reached their ATHs again.

The market has inertia. What goes up usually continues going up and what goes down usually continues going down.

If you bought Yahoo at 20% below its peak value, the fact the company still exists two decades later isn't much consolation.

Not saying there isn't shady stuff going on too. There definitely is, but even if there wasn't it is a skill based game.

This hints at some sort of deserved meritocracy that just doesn't exist. Funding is king nowadays when a large fraction of trades happen via HFT. Implying that all you need is knowledge in order to reach wealth is misleading at best.

Most of the smart money is in hedge funds anyway.

https://12ft.io/proxy?q=https%3A%2F%2Fqz.com%2F2108874%2Fthe...

Sure, $1,000 to $85,000 is a great performance, but not life changing in itself.

I just posted this to show that at least the math can work even with extremely small amounts. Having lots of capital only buys you lower and lower risks.

This book explains what the stock market actually is: https://www.amazon.com/Flash-Boys-Wall-Street-Revolt/dp/0393...

It's much less friendly than it seems and only "efficient" for a select few.

- Michael Lewis really only got one side of the story - that of Brad Katsuyama, who had a vested interest in casting HFT players in a bad light to promote his own business - building the new exchange IEX.

- Brad also blamed HFTs for systems at RBC failing to make massive trades like they used to. There was nothing nefarious here - RBC had just fallen behind the time in technology, like trying to send a Fax in a world where everyone already uses Email. If Brad, or RBC, or RBC software engineers picked up the phone and called any of the exchanges, they would probably gladly update them on the industry and save them all the work of re-discovering it themselves.

- The claims about front-running are completely false. Front running would mean that a market maker somehow knows someone's orders at two different exchanges and somehow is able to "get in front of the line" or even know that those orders belong to the same person. This would mean the exchanges leak information or allow certain users "ahead of the queue". None of this is true. What Michael Lewis called front-running, was HFT firms reducing their risk on other exchanges when they would get traded against on one exchange. They did this without any knowledge that Brad Katsuyama was on the other end, or that he was just late trying to make the same trade at another exchange at a later time. There are no guarantees that you can make the same trade at different exchanges - the same rules apply to everybody.

- Unsurprisingly, IEX as an exchange is no different from others, in that they need market makers (a.k.a. HFTs) to provide liquidity on their exchange. I wrote the code for the FIX gateways to connect our firm to IEX, and it was all business as usual.

"Front running" as defined by the SEC has a more narrow definition. It basically means that you have a customer that has placed an order for XYZ and you aware of the order, but you placed your own order to be executed in front them, thus forcing them to buy it from you at a higher price than if their order was executed first. HFTs are not "front running" anybody.

{kind=link}