Importantly, none of these businesses are using crypto because it's crypto or for any speculative benefit. They're performing real-world financial activity, and they've found that crypto (via stablecoins) is easier/faster/better than the status quo ante.

Bitcoin (and possibly a few others) is one of the few uses of blockchain that actually makes sense. The blockchain serves the currency, and the currency serves the blockchain. The blockchain exists to provide consensus without needing to trust any off-chain entity, but the blockchain relies on computing infrastructure that has real-world costs. The scarcity of Bitcoin (the currency) and arguably-fictitious reward for participation in mining is the incentive for people in the real world to contribute resources required for the blockchain to function.

Any real-world value given to Bitcoin is secondary and only a result of the fact that (1) mining infrastructure has a cost, and (2) people who understand the system have realized that, unlike fiat, stablecoins, or 1000 other crypto products, Bitcoin has no reliance on trusted, off-chain entities who could manipulate it.

You trust your stablecoin's issuer that they hold enough fiat in reserve to match the coin? You might as well trust your bank, but while you're at it, remind them that they don't have to take days to process a transaction - they could process transactions as fast as (actually faster than) a blockchain. But I imagine most banks would point to regulation as a reason for the delays, and they might be right.

So what are stablecoins really trying to do? Circumvent regulation? Implement something the banks just aren't willing to do themselves?

And it sounds like this system targets global payments. Does that imply that some day users would be able to pay using Tempo? Where would we see Tempo?

Very genuinely curious.

I don't think that customers or businesses should see Tempo very much. In the success case, Tempo is a platform like SWIFT or ACH that others employ behind the scenes to orchestrate transactions. "Decentralized, internet-scale SWIFT" isn't exactly the right analogy (there are clearly lots of differences), but it's not totally wrong either.

Why are businesses finding crypto easier/faster/better?

Yeah, I think this is the natural follow-up question. The answer differs a bit based on the use-case, but there are a few common reasons:

* Instant on-chain transfers avoiding trapped liquidity. If you're transferring money from financial institution A to institution B, and the transfer takes a day, you're either slowed a day in taking the next step or you have to somehow cover that float. Depending on your movements and their predictability, that can require big buffers.

* Fees that are lower than cards. Card payments are instant, which is often valuable (and superior to many bank transfers), but card transactions are also expensive relative to stablecoins. (And while card authorization is instant, settlement is not.)

* Reliability. This sounds funny, but, when sending money between countries, there are many more manual processes involved at the associated financial institutions than one might think. Money is frequently just... lost, and humans are required to hunt for it. (We see this all the time at Stripe.) Crypto is punishing if you make a mistake, but, if you do things correctly, reliability is all-but guaranteed.

* Fewer currency conversions. Wholesale FX for major currencies is very cheap, but minor currencies can have bigger spreads, and the actual fee incurred by a regular customer (e.g. with their bank) can be significant. Stablecoins often make it possible to skip conversions that would otherwise happen.

* Access to USD-based functionality. The US is the world's most sophisticated financial services market. Having a stablecoin means "having an on-chain asset", but it also typically means "having a USD asset", and a lot of major parts of the ecosystem (e.g. US equities and credit markets) primarily, or only, deal with US dollars.

Acknowledging the obvious, a reflexive answer frequently invoked here is "it's regulatory arbitrage", but I think this is some combination of misguided and incurious as an explanation. First, stablecoins are now formally regulated in the US (with the GENIUS Act) and in Europe (under MiCA), so their use is now very explicitly regulated. Secondly, it implicitly assumes that the only reason one would seek an alternative to the traditional ways of doing things is because someone is doing something illegitimate. I think this usually indicates a lack of understanding of the challenges, complexities, and costs associated with high-volume cross-border money movement. Indeed, and somewhat ironically given the claim, one of Bridge's large customers is the US government.

Today, if you want to transact between businesses or retail (folks like you and I), you need to find a route between the two entities' banks. This route might take several hops, passing through some central banks, and some of these hops might be instant or might take days to actually settle. On top of that, you need to pay the service that helped you find a route (SWIFT) and potentially the nodes your transaction goes through. Bottomline, it can be slow and a lot of middle men are taxing you.

This is why you see services like (Transfer)Wise, that basically try to bank everywhere, and allow you to send money faster by taking a shorter route (kind of like a wormhole :D). But they have to add liquidity everywhere, which they have to rebalance constantly, and it's centralized (single point of failure). FWIW it's great because for a long time this is the best thing we had.

Now, let's take a look at the other side. Using stablecoin is a matter of just creating a wallet. The openness by default of blockchains make it really easy to integrate with a blockchain as an entity (just use the SDK, it's there by design). Furthermore, it's in many cases instant and cheap (unless you're transacting on a slow blockchain, but then that's your fault).

That being said, the elephant in the room is that one stablecoin (let's say USDC) is now present on many blockchains. So if you have USDC on chain A, and I have USDC on chain B, we're back to our "tradfi" world where we have to find a route between our two chains, which might take us over many bridges, which can be slow and costly. The alternative, like with Wise, is to use centralized players who have liquidity on many different chains and can move things around by just updating their internal (and centralized) database. It's tradfi all over again :D

- SWIFT is really just a messaging protocol between a distributed, decentralized set of global banks that are all passing messages/money between each other. Your SWIFT wire might pass through an arbitrary number of correspondent banks, sort of like a flight route with multiple stops, until it reaches its destination.

- Consequently: money moves slowly (up to 5 days), is expensive to move (variable fees assessed either to the payor or payee, by every bank in the chain), and there is an indeterminate amount of manual ops burden, multiplied by every bank in the chain.

- As another commenter points out - services like Wise really just use massive amounts of liquidity spread out globally to try to minimize the number of true, bank-to-bank cross-border settlements required to get low-value payments from A -> B internationally.

Ironically, I think the great accomplishment of stablecoins is its "centralizing" of cross-border money movement into a single ledger -- reducing it to a "book transfer" of sorts -- where getting all the world's money to pass through a single ledger would otherwise be a very difficult (probably intractable) challenge _if it were not for_ the permissionless-ness + global neutrality of the blockchain that is tasked with doing so.

(I wrote about this in a slightly longer post here: https://text-incubation.com/The+great+irony+of+stablecoin)

I chose wire transfer. Which meant going to my bank, getting approval to get paid, fill out two forms, and making three total trips.

I now have contractors in Nigeria and Philippines who want to get paid in USDT. It's instant and there is a thriving local scene of P2P sellers for instant liquidity.

One way to see it is today the EVM ended up being the solution to a lot of other problems.

The banks are dying, their core banking is dying after 50+ years of service. There hasn't been any real investment since 2008, only minimal maintenance and cost cutting. Also generations of incompetent people at every levels created a situation with no escape.

Also things like SWIFT became very irrelevant in practice. I can assure banks did not really used it for a while.

When Ethereum and its EVM appeared 10 years ago a lot of people saw an opportunity to build a better "programmable money" platform but nobody really succeeded. At the same time Ethereum did not fail, improve and still secure the assets and run the smart contracts deployed in 2015. More than enough to convince the people on a sinking ship to jump on that boat.

My guess is the the EVM is becoming something similar to UNIX: a loose standard almost everybody will build on. Maybe not the best but something good and flexible to jump and we need to move forward.

Also the dollar urgently needed a new outlet so its on.

So it is not really about "crypto" it is more about the EVM as a platform.

From the example given from Argentina, it bypasses capital controls, which until recently, made accessing foreign currency very hard/expensive/illegal. Argentina had a huge crypto boom because of them.

A regular log or ledger file could accomplish the same thing as a blockchain for significantly less technical debt or ongoing expense.

And note that the best use cases Stripe could find for "real world" use cases were a company trying to complicate its FX cash management, and a cash transfer app with fees higher than most of their competitors.

here is what you're missing, and is very easy to miss:

the third party, unaffiliated, developer experience is better on an EVM than it is is on a traditional centralized database. Than it is on a shared database with a bunch of signers. Than on any "web 2.0" cloud platform. the developers continue to bring their entire audiences with them, even though those audiences are quite small, they've grown in aggregate to be large enough.

in web3, of which EVM platforms dominate and are the most mature, there is a tiny payment for deploying your application once, and then it exists in perpetuity for free at unlimited levels of bandwidth. your users pay to update the state of your application, and in many cases you can earn from them doing that.

there is absolutely nothing in the cloud world that achieves the same thing at the same cost. the payment paradigms are entirely different, you have to pay for hosting, deployment, the thing that handles your deployment, additional workers to unbottleneck your continuous deployment, the bandwidth, bandwidth spikes, and get nickel and dimed on a ton of more things, or paying a premium to a service that handles all that for you.

additionally, the concept of "composability" is attractive in the web3 space, again spearheaded by standards on EVMs, the concept is that third party applications are automatically compatible with each other. there are infinite permutations of combinable operations one can do or enable amongst deployed applications. you can compose, or combine, applications in a far less cumbersome and less fragile way, than with REST and APIs of different people's apps in the web 2.0 world.

and on top of that, if one of those permutations becomes useful and you make it user friendly to do so, you can collect a toll for others doing that operation. this is just financial services, where "basis points" are collected by intermediaries.

a common application are forms of lending. initiating borrowing, trading the opportunity, and closing the loan within a split second, leveraging 3 - 10 financial services at once, is something that's better faster and cheaper than what has been possible outside of the blockchain space. the ability to do so is gatekept by the other financial industry and payment rails in ways that are no longer necessary to debate. now you can do these things with $3 in capital instead of needing $3 million dollars to pursue getting an API key from some old slow moving organization.

the compelling reason to create a new EVM are to change some basic parameters. block time, the size of contracts (the aforementioned operations) that can be deployed, and which standards are included into that chain, and of course the governance model - how are new standards deployed and how are transactions added. making stablecoins a first class citizen would need a new blockchain. how your governors/validators/nodes and RPCs function under load would need a new blockchain.

it is very attractive to developers that they can deploy applications "in the cloud" that have a very nominal cost, doesn't cost them to maintain even amongst spikes in bandwidth. they don't have to incorporate or do any formalities while having unlimited financial upside, solely because there is already hundred of billions of dollars in notional value sloshing around in that space to cater to already.

edit: I'd actually like to work with Stripe or other web3 organizations again on these kind of applications, now that I notice how boutique it still is to understand what's going on, email in bio

That's more or less exactly what this is. Stripe is launching an EVM L1.

The Ethereum Virtual Machine part gives it a mature tech stack with experienced developers and auditors. Plus, well-tested smart contracts that have already processed billions of dollars on other chains can be deployed on Tempo.

The "Stripe L1" part will ensure that it's fast, simple, near zero cost.

Indeed you can! We even have a name for that! Its called a blockchain.

> This maintains many benefits of the blockchain and lacks many issues (fast, simple, near zero cost, controllable to a given extent -- no takeover possible, ...).

Blockchains can do all of these things.

Perhaps you are thinking of "bitcoin", instead of "blockchains"? Bitcoin, something that was created a whole 17 years ago, indeed has many drawbacks compared to modern blockchains.

[1] https://docs.google.com/document/d/1L0Me9si4iMclOq8n-oG2yNQf...

I'm guessing the GENIUS Act had something to do with it too? Now that bank depositors have an incentive to hold bank-issued USD stablecoins given their priority in cases of bankruptcy[0], it seems likely there will be a lot more transactions with them as well

0. https://www.congress.gov/bill/119th-congress/senate-bill/158...

You mentioned sub-cent tx fees, 100k tps, and what I presume to be atomic swaps for stablecoins. Are you thinking about something like $0.10 fees or something like $0.0001 fees? At $0.10 fees at 100ktps that end up representing $100/s in tx costs which is about $8.6M/day or $3B/year. Presumably you expect to make more per year on this project in the ideal case, so are you intending to allow the fees or TPS to "float" upward, or to restrict participation in the L1 to only trusted partners, or for the network operators to make money off the interest from holding the stablecoins' currencies in reserve? What if demand exceeds 100k tps?

Since this will be a corporate backed project how do you plan to handle sanctions and government currency controls, eg if Uncle Sam tells you to drop support for Iranian currency, how will that work?

Will there be account/transaction privacy built into the network through ring cryptography or zk proofs? I'm assuming no, but if your answer is yes and Uncle Sam takes issue with that, what is your plan?

But as long as I don't see somewhat more transparent conversations with the people in your orbit like patio11, Matt Levine, Kyla etc, where you address how you'll actually tackle the non-technical challenges ahead, this GTM communication and site looks like every other 2019 JPM, HSBC etc "something blockchain" announcement and hard to get behind as something that might as well be really different this time, and not be killed/sidelined by vested interests. Including your own.

I completely understand that there are markets and customers that can find real utility in it, but I wonder how many businesses will really ever benefit from stablecoins.

We're in higher education, and potentially our international clients could avoid hiccups with regulation, delays, compliance, and more using stablecoins, but it's really a guess. In the meantime, the pricing model of stripe seems to prioritize bigger and bigger clients.

That being said from Stripe's perspective stablecoins an easy bet to make. They win by building payment infrastructure within the traditional payment ecosystem and win by providing an alternative completely outside of it.

Checks crypto watch, ah, it's Latin America time again.

A little bit of trouble coming up with enough examples of anyone who wants or needs this, I think?

When your algorithm freezes a legit business's funds, you hold them indefinitely and can invest them for your own profit. The only recourse you offer is mandatory arbitration with an arbitrator Stripe chooses.

How is that a fair system?

"A diverse group of independent entities, including some of Tempo’s design partners, will run validator nodes initially before we transition to a permissionless model."

I think Zuck tried to do this. It was called Libra or Diem or I can't remember what it ended up being. Ultimately trust is what matters. In the end whether it was regulation or governments or anything else that killed it, it's only going to work if people can trust you. They trusted you with fiat payments, maybe they'll trust you with crypto. The thing to note, you'll win over the US centric crowd but it's unclear if it will translate truly across borders to Europe, Russia, China, etc. I'm guessing that doesn't matter but just remember what happened. Make sure to be honest about who's actually going to run the payment rails here.

It must be ignorance on my part or perhaps I’m just lucky with residency and clients, but I get paid through services like Wise frequently. Taxes are pretty reasonable and I receive the money instantly on my bank account from US, Europe or Latin America. I don’t really know much better it needs to get.

I can never understand what problem stablecoins are trying to solve.

Even just paying a foreign contractor is a pain in the ass sometimes so if a bunch of banks and financial service providers around the world manage to make international transfer easier via the coins, that’s great. Not everyone cares about the inconvenience of KYC or reversibility of transactions sent internationally. These usecases feel more like shortcutting the complexity of transactions across state lines rather than the regulations we’ve learned about the hard way in a hundred years. Obstacles rather than safeguards.

As someone who actually worked on some crypto project (nanotimestamp) and also has got paid in crypto. I usually just convert it into stablecoins / gold coins for a short term (1 year max) where since I am still a minor, I don't have a bank account and so I mean, the end goal is to get my stablecoins out of the chain into real money not vice versa.

I had written something like this, just with a clickbaity title but its basically that I hate everything in crypto except stablecoins which I really like. Like there is paxgold which has gold and I genuinely like the fact that I think that we might be able to pay in gold or etc. stuff, I also like USDC too.

Here's my article: https://justforhn.mataroa.blog/blog/most-crypto-is-doomed-to...

This doesn't really help that.

KYC isn't an 'inconvenience' it's a legal requirement that you (or your employee) can go to jail over if you do not comply with.

Or can you explain how these bike importers are being hampered in fiat not by laws, but by technology?

Every time I look at this, the "clever trick" is actually law evasion / law avoidance, to borrow a tax term.

It's about as "clever" as lying to the IRS to save money on taxes. That was never a loophole.

Are you tracking all of this for tax purposes? These transactions all have to be reported to the IRS even for stable coins. This is the biggest thing making crypto payments a non-starter. What's the story here from the end-user's perspective?

I as an individual have no interest in stacking stable coins if when I spend them to businesses, I have to meticulously track each transaction and report it. Whatever you're doing for businesses doesn't seem like it would solve this problem for individuals, if you're even solving it for businesses themselves that is.

Did you look at a non crypto/stablecoin solution to perhaps find something even better for legitimate businesses (and perhaps worse for crooks)?

Using crypto to dodge currency controls?

Of course I agree that currency controls are bad. But, if the use case for crypto keeps being fostering illegal transactions then it doesn’t solve anything a functioning economy needs.

To add some context: our clients in LatAm use DolarApp to spend internationally with a card at the best rates, send and receive cross-border transfers (not just remittances, but also payroll), and to keep their savings pegged to the dollar. Stablecoins let us deliver a much better user experience and significantly lower fees — in some countries, up to 10x better than incumbents.

That said, most of our users don’t care about the underlying infrastructure. They care about the benefits. It’s similar to how someone using a bank card at an ATM doesn’t know (or care) that the system might be running on COBOL.

We see it as our job as product people to absorb that complexity so our users get the benefits without having to deal with the complex mechanics behind them. That’s what we believe is helping unlock a platform shift.

One sign of a technology becoming mature is when it stops needing to be the main character. It starts to make room for what it does, not what it is.

When thefacebook launched, it wasn't a PHP-based social network; it was a social network for college students.

Blockchain has been the main character for a very long time and it's really encouraging to see a product launch like this. Congrats to everyone involved in making this product a reality.

I still don’t quite understand the point of using crypto then - there’s no advantage in it theoretically being decentalizable since practically it is not. It might as well be an implementation detail.

Or are there decentral aspects to how it works? Does it ease auditing? Is it the improved ease of financial/regulatory engineering?

SpaceX using crypto? Are any of their customers seriously going to pay using crypto? Are they gonna pay any of their bills using crypto? I'm not trying to piss in your Cheerios. But making real world use cases not die of uselessness is going to be a challenge.

1.5%

$0.045 per credit transfer

$0.01 per request for payment message

$1.00 per liquidity management transfer

BTW, it is crypto. So the promise that none of these businesses are using crypto because it's crypto or for any speculative benefit is a provisional promise at best. Hyrum's Law argues an opposite future.

- It rang a bell but I had to look it up, figured I'd share to save others the trouble.

https://www.wired.com/story/genius-act-loophole-stablecoins-...

I can less immediately expand "easier" and "faster".

Easier: on chain VMs are far from simple or easy, recovery from mistakes is far more complex. Some other aspects such as the implicit common standard might reduce some amount of need for "green field agreement", and the implicit openness of the protocols avoid some of the traps of "here's a rest api, go", but is this the focus? When you look at a wide variety of the big ticket items in everything that needs doing, is the total set easier? Are there surprises there?

Faster: similar to above, this claim is surprising. There's a lot of by-design overhead to a cryptographic ledger system. Lots of things that can be done to make it wider, to reduce latency and increase throughput, but at a fundamental level core operations such as transaction creation require a lot more processing going into a ledger than into a traditional database, even one at scale. Maybe faster here isn't about system faster, but time to product delivery? If so is that common standards? Are there surprises here too, what were they?

Edit: I see elsewhere in the thread you provide some answers in a slightly different framing. A potentially unfair paraphrase and summary seems to be that this enabled integrations to bypass expensive incumbents and comparatively poor traditional infrastructure. If that's a reasonable approximation my question is this: what if you dropped good sized chunks of the blockchain part that is the main system bottleneck, but kept the rest of the properties (shared micro computation model, shared transaction model, common API standard and protocol, eradication of foot dragging incumbents etc).?

Long term I'm still more optimistic on crypto than AI. I think part of the problem with crypto is it needs to be around longer than some government money to prove to people it has staying power. Only then will financial people start doing things like recommend a small crypto stash for your retirement just in case. The average person is not going to make the necessary critical mass move into crypto without some sort permission saying its ok and not going to risk all their money or jail time.

Do they use it to arbitrate NFTs? (need more jargon)

Because SpaceX is definitely something that screams "finance" to me.

> Private blockchains are completely uninteresting. (By this, I mean systems that use the blockchain data structure but don’t have the above three elements.) In general, they have some external limitation on who can interact with the blockchain and its features. These are not anything new; they’re distributed append-only data structures with a list of individuals authorized to add to it. Consensus protocols have been studied in distributed systems for more than 60 years. Append-only data structures have been similarly well covered. They’re blockchains in name only, and—as far as I can tell—the only reason to operate one is to ride on the blockchain hype.

In particular, using the term "blockchain"/"crypto" to talk about something more centralized / permissioned than e.g. Bitcoin is missing the point: these systems already existed before.

So what do you mean by "crypto" exactly? Distributed systems? I don't think you'll find many distributed systems skeptics on HN.

It's inevitable that agentic AI will handle a lot of workload online eventually. We can't expect these agents to work on existing payment rails, what with their fees and slow settlement and international payment hurdles.

AI agents that can pay each other when necessary - even tiny fractional amounts - will be a massive use case.

People can build their own smart contracts and speculate.

Does Stripe have a perspective on the unique systemic risks that stablecoin exposure might end up having in the new regulatory landscape?

I genuinely do not understand this example. What is spacex actually doing? And why do they even have money in “long tail markets” at all?

Otherwise why not just use normal digital payments? I fail to see why a blockchain is needed to log the transactions.

That's part of it, but:

1. Progress often depends on evolving obsolete regulation.

Uber works much better than taxis (once upon a time, people could "call a dispatcher" an hour in advance, wait on hold, etc) and yet in the early years they had to work around taxi regs.

2. Blockchains are a fundamentally more robust way to run a ledger.

If any of you have ever written software touching tradfi custody you'll know about "reconciliation"--start of every business day, you get a dump of files in your FTP server in various proprietary formats. You parse the transactions and they don't add up. The Recon team hand-corrects and recategorizes edge cases so that the balance deltas match transaction totals and everything ties out.

This type of absurd duct tape is ubiquitous, and it's a major reason why trad rails have multi-day settlement times and even longer for international. Inflates team size and cost required to run a product. SWIFT is a messaging system -- bankers use it to essentially text each other about wires to figure out issue resolution. Some lower-level trad payments regulations are written assuming that this level of manual oversight is required to prevent ledgering errors and ensure sound accounting.

Stablecoins run on transparent, precise ledgers with machine consensus. This doesn't solve everything, but there are large categories of issues that can occur in trad payments that do not exist onchain.

3. Control is liability.

Some important regulations actually encourage blockchain-based payments. For example, money transmitter law places significant requirements on custodial money transmitters (you take money from Alice, with a promise to give it to Bob) that do not apply to noncustodial channels (you give Alice a mechanism to send directly to Bob).

I’ve heard stable coins are beneficial for the owners of the coin because it’s basically an interest free loan to the token owner.

So I get it I guess!

Edit: I’m only joking a little bit

The website is a bit painful to read but I thought it provided good general information for potential partners.

As as a dev, my questions are why did your team decide to build a new L1 chain instead of an Ethereum L2 and why did you all stick with the EVM architecture instead of looking at something like the MoveVM?

One can look at Stripe's list of investors...

By shifting flows onto a private stablecoin ledger, Stripe isn’t fixing inefficiency; it’s making it easier to route money in ways regulators and tax authorities can’t easily monitor. That’s not innovation, it’s the oldest trick in the crypto playbook: pretend you’re improving payments, when what you’re really selling is a way around the rules.

You just can't "invest" in this vision just as you can't "invest" into treasuries, I mean you could but they don't give 100x the returns.

I skimmed through and I don't see anything that promises a lot of returns and THAT'S A GOOD THING. Just like how things like (okay, I was thinking of some universally loved non ipo company and I thought of silksong which is going to get released, so team cherry!!) So if you want to invest into team cherry, the best you can do right now is maybe buy the game but that isn't investing I think its in the similar manner and its a good thing since it prevents frauds and false returns advertising

There is (usually) no free lunch. Nothing that can give 100x returns anyway, there is insane competition on things like on beating the market consistenly even with 1% is really hard and only very few companies do and even then, their past record doesn't indicate the future remains the same. Tldr: I am that salesman of index funds. also diversify, s&p have a huge concentration on AI stocks and so please diversify into world stocks or maybe even more into non american stocks since american markets are heavily focused on AI and I doubt that it will play out since the markets do feel like they are in a bubble right now

I'm not surprised, capital controls come and go there, and when they come, they stay for several years.

https://www.linkedin.com/posts/jasonmikula_fintech-partner-a...

When this bank employee expressed skepticism of "DolarApp" he was faced retaliation:

https://ia800508.us.archive.org/28/items/gov.uscourts.flmd.4...

"10. In and around the spring of 2023, Mr. Ibrahim became uncomfortable with certain practices and activities in which the Bank began to become involved. These included practices that, in Mr. Ibrahims opinion, jeopardized the Banks compliance with anti-money laundering laws, federal safety and soundness requirements for depository institutions, and compliance with specific OCC regulations and requirements that were particularly imperative due to the fact that the Bank was already considered a Troubled Institution

14. Mr. Ibrahim further objected to Axioms initiation of new business programs, without first obtaining non-objection letters from the OCC and without review by the Banks internal New Product Risk Committee, as required by written policies. One such project, DolarApp, was of particular concern to Mr. Ibrahim as it entailed cross-border movement of funds, which triggered significant concerns as to whether the Banks BSA/AML controls are sufficient, among other things.

15. But when Ibrahim raised these concerns with the CEO, Ross Breunig, he told Ibrahim to the effect that he did not want to hear it and shut down the conversation.

18. Almost immediately after Mr. Ibrahim objected to these practices, Axiom and Mr. Breunig began a pattern of retaliation. After the April 2023 leadership meeting where Mr. Ibrahim raised concerns relating to CSI and the DolarApp, Mr. Breunig began canceling Executive Board of Director meetings that Mr. Ibrahim attended.

19. Following a leadership meeting in May 2023, where again Mr. Ibrahim raised concerns about CSI, DolarApp and the overdraft positions, Mr. Ibrahim began receiving email cancellations to multiple committees and Board meetings.

20. Upon inquiry, Mr. Ibrahim learned the meetings were not being canceled, but rather he was being uninvited without explanation. Mr. Breunigs hostility with Mr. Ibrahim also became noticeably apparent during this time."

Of course Stripe, Inc. is neither a Troubled Bank nor an untroubled one

Anyway, it sounds like DolarApp could be useful for evading anti-money laundering and bank secrecy laws

"Importantly, none of these businesses are using crypto because it's crypto or for any speculative benefit."

That's only one of the many reasons people might be skeptical of crypto. See above

"They're performing real-world financial activity, and they've found that crypto (via stablecoins) is easier/faster/better than the status quo ante."

How much of this "real world financial activity" is not criminally culpable

100% no doubt

You could achieve the same things with a proof-of-authority ledger instead of a "stable" coin

Stripe processes a LOT of money. The customers that get that money need to move it around. Often to banks. Stripe makes no money on that.

Over the last few years, stablecoins have become a preferred means to hold and move money (for convenience, etc).

Stablecoin providers make money on their float -- selling stablecoins means you get free deposits, and risk-free rates are presently around 4%. For every $1M in stablecoins your customers hold, you can make $40k/year. Stablecoin providers like Circle pay about half of that back out to partners that sell the tokens.

Stripe is huge, and well-trusted by customers for handling payments. By adoption stablecoin infrastructure to control financial flows into stablecoins, they can amass huge amounts of stablecoin sales.

If even ~3% of their transaction volume gets held in Stablecoins, and they make 1% a year on that, it's about $1B a year in bottom line.

~$10e9 (daily avg vol) * 365 * 3% (converted to stablecoins) * 1% (net income) = ~$1B

For avoiding regulation.

Part of the very high level play is the US Govt seeks to diversify away from depending on nation states for borrowing, and to promote tech companies to the status of reserve holders.

This doesn't add much to the consumer however. I think in fact we are looking at a "fragmented currency" future where you hold like 36 different stablecoins in your wallet because certain platforms accept certain stablecoins. The GENIUS act doesn't offer strict guarantees for getting out of a stablecoin into USD, so I predict dark patterns and "incentives" to make it hard to get out of a stablecoin.

I’m typing this shortly after buying my groceries with a visa debit card that was funded 30 seconds before the transaction over Lightning Network with Bitcoin that was sold at a 0.1% fee for USD and immediately then transacted on Visa debit payment network.

The reason banks are lobbying so hard recently to close “loopholes” in latest US legislation is because with stablecoins you even need them less and less to hold dollar exposure.

The days of traditional banks are likely numbered and the crypto skeptics commenting on HN have their world models upside down. At least that is my view currently.

[1] - https://coingeek.com/tether-bitfinex-prohibited-from-operati...

[2] - https://ecoinimist.com/2024/09/20/concern-over-tether-audits...

[3] - https://finance.yahoo.com/news/sec-fines-tether-former-audit...

These numbers only work while short term rates are high (relative to recent history) and the share percentage is low. The lower the rates and the tighter the margins, and it drops like a rock.

Nobody with a sizable balance is going to accept the risk of a system like this without being paid a premium over traditional bank deposits. If my bank gives me 4% I’m not going to give stripe half of that in exchange for losing FDIC protections.

Huh?

In the western world this is nonsense. I move 6-7 digits regularly, internationally, even between continents, for free. Convenience of cryptocurrency? Lol. Maybe if I want to send money to Nigeria or North Korea.

Cryptocurrency was never more convenient. It's cheaper than Western Union when that's the only alternative, but boy is that a low bar and an edge case.

Traditional banking is getting faster and cheaper by the year, so your claim is getting less true every day, not more,

They do if you charge in a foreign currency, e.g. in USD and transfer it to the bank account abroad, e.g in CHF.

Moving money, sure. Holding money, only for chumps. The oldest grift in the cryptocurrency book is "unpegged no-audit stablecoin" and vanishingly few tokens actually put their money where their mouth is. Anyone can spin up money out of nowhere, but only a few businesses can survive a true bank-run scenario.

This seems like a threat to put pressure on CBDC to be pro-business or else the private sector will take over part of their job for them. A rational administration would probably want to put a stop to this, letting the private sector print it's own money will invariably end in heartbreak.

I'm not in that space, but how stable is that 4%? What is it correlated to?

The US gov let Circle be a less-regulated bank than other banks. This is called "regulatory arbitrage". You can take advantage of it by checking the box that you have a "blockchain".

Stripe noticed "wow, things labeled blockchain are nice for some people to use" because of this dumb inconsistent banking regulation situation.

Stripe doesn't mention that the underlying tech is impotent, they just have to play along, and here we are.

I think it is useful and is here to stay

Okay, so one: Obviously pointless from a tech POV. There is nothing that a Stripe controlled blockchain could offer that a database could not.

But then, why? Sadly, as someone who does like the ideals of true cryptocurrency, yet another way to make sure "real" crypto doesn't happen, much like what is happening to BTC.

Here's hoping (yeah, it's a long shot) people see through all of this and maybe, MAYBE, get into the actual ideals of cryptocurrency again.

One way of thinking about a blockchain is to think of it as a shared datastructure to keep databases in sync. Any time you want to distribute your database over more than just a single central place, in a cryptographically secure way, you're probably going to re-invent a blockchain to do it.

Even more specifically, a blockchain is for when you want Byzantine fault tolerance, i.e. you don't trust one or more of the actors involved. This is the main distinguishing feature of blockchains IMO, the reason we have proof of work, proof of stake, etc. It's also the main thing I saw people getting wrong when using blockchains during the earlier waves of cryptocurrency fever; most proposals for blockchains did make sense as distributed public ledgers, but didn't really need the extra computational overhead because only trusted parties were adding blocks to begin with.

Stripe, nor any other bank or bank-esque thing needs this because they have already well solved their problem of "trust."

"Blockchain" is pointless overhead here.

blockchains solve a self-invented problem

A database cannot resist tampering by somebody with admin access to the database. It may be the only thing that blockchains have going for them, but it's a big one.

Never trust a cryptocurrency developed by a for-profit corporation.

Oh, wait... I've been handed a piece of paper...

Because I feel pretty confident that it is dwarfed by the volume of money that has been unlocked by tying crypto to ransomware.

There absolutely is. Its called having access to the ecosystem. The money features that exist in the current blockchain landscape are simply a better developer ecosystem, with many more features, than the non existent "Database driven", uhh money tools.

Blockchains are no longer about the singular feature of having a trustless ledger that bitcoin tried to provide. No, instead it is about a whole variety of money related features and developer ecosystems that simply do not exist outside of the crypto space.

Recreating all that exists in the crypto space, but using a database instead, sounds like a lot of wasted work when you can just use the tools that are already available.

It's not for lack of trying that traditional, "database driven" cross-border payments are costly and unreliable. SWIFT have thrown technology at this problem: GPI, Swift Go, ISO20022, etc.

Unfortunately the ecosystem has an extremely weak technical culture. Banks rarely follow the standards as written – your perfectly crafted API payment may be re-keyed by a low-paid human operator on a slow, buggy UI written a decade ago.

I could believe that the developer experience and technical standards of the participants is where the value lies right now.

The one thing I'm not sure on is to what extent those ecosystems depend on reduced regulatory scrutiny compared to banks.

None of those things require a blockchain and are all made less efficient by doing them that way.

Again, truly decentralized cryptocurrency ADDS slow clunky overhead; that's the price of decentralization. Everything you're imagining is ALL done much easier with good ol' databases et al.

Are you claiming here that things like banks and stock markets don't exist?

Genuinely curious though; what kind of 'money related features', that have no non-crypto counterparts, are you referring to?

Like what? Speculation?

All these people harping on about: "Bro I just need to move my money without trusting anyone!, I just need a trust-less way to send currency bro!"

Trust is a good thing! Banks and financial middlemen aren't the devil. Look at how many TPS the visa network can do thanks to trust.

If it weren't for some minimum of social/institutional trust the whole of society would collapse anyway and your digital coins would finally converge to their true value (zero - or actually negative once you add in the externalities).

I’m curious to know more.

Thanks

The others aren't doing well right now despite the fact that the tech that runs them can do what crypto promised, often better. It will all come down to whether people will buy in?

Stablecoins require trusting that the coin issuer doesn't print money. This goes against the core premise of blockchain being trustless!

This is just a payment API with extra steps (all of the integrity and identity features use cryptography that works without blockchain, unless your definition of blockchain is broad enough to include git and matrix chats, then the stripe thing is a blockchain too).

https://www.irishtimes.com/business/technology/stripe-takes-...

The reason Stellar was appealing was because Stripe invested into it. I wonder if Tempo is using a similar consensus mechanism as Stellar (and/or Ripple)

If Stripe’s closed-loop system scales, banks and card networks could lose significant transaction volume, fees and even merchant relationships. Merchants and customers win with lower transaction fees. This marks a very credible and large-scale effort yet to challenge the Visa and Mastercard duopoly.

Obviously not perfect and other questionable projects have stained blockchains reputation but it is a net win, no?

Blockchain is used as an umbrella term to lump useless systems like this and ripple into the same category as actual decrentralized cryptocurrencies.

I am actually optimistic that, finally, there could be a convincing answer, because stripe does not strike me as the type of company that would do this without a very good reason. (I am slightly less optimistic, because the page itself does not offer an answer to this question, and instead argues for tempo against other blockchains. But only slightly.)

I will end with this thought: If we can get to a new local equilibrium where global transaction costs are 10x lower and >30% of global GDP can get paid faster / with better price signals / etc., shouldn't we try even if the tech is non-optimal?

Stablecoins are a sort of “glue” between global banking infrastructure that otherwise would be difficult to set up as a provider (due to regulation), slow (due to bank technology for global payments being slow), and opaque (due to the shortcomings of global payments between financial institutions).

If the goal here is to overcome regulation isn't all this threatened by the possibility of new regulation that recaptures this behavior?

The conventional system is slow, insecure and does not interoperate well because of regulation.

This whole scheme is just dressing up a centralized payment provider as a cryptocurrency to avoid regulation for a short period of time.

I mean FFS the dang tokens are literally pegged to the dollar.

I don't really get the draw either - what is the point of having a distributed blockchain if it is controlled by a single entity?

"EVM-compatible, built on Reth" => they're essentially building a private Ethereum fork with a fancy validator selection process.

Couldn't they just get these benefits (predictable fees, fast settlement) by ... running a database between these financial institutions?

If Stripe controls the validator set (even indirectly), then ... just a distributed database with extra steps, no?

Sure, but they wouldn't get all the legal and regulatory bypass benefits of using cryptocurrency.

To have deployed some blockchain layer 1 nodes, it's actually quite similar than deploying a distributed database.

Nowadays, it's actually just easier to fork geth/reth or other engine, and just deploy it. There are so many doc and tooling that can then be reused.

Fancy validator selection sounds like the individual financial institutions are still responsible for managing and maintaining their nodes, which gives them a fair (as in balanced not fair as in a lot) amount of liability/responsibility/control.

A distributed database, afaik, while geographically distributed, entails more centralization of power/control.

They cut out a lot of work for themselves expecting stable coins to materialize on their own chain. It's Stripe, so maybe they are allowed to mint their own USD stable coin, but that's one coin. They might have been better off making an L2 on Ethereum. Otherwise they are going to have to run Uniswap in their EVM implementation and hope that liquidity shows up.

I can see Stripe's customers wanting to use a solution that just works and is backed by Stripe's own distributed ledger, but I can't see their customers' customers wanting to do the same. Their customers' customers are going to want liquidity to other tokens, and privacy. At this point I don't think that a payments protocol can succeed unless it provides privacy comparable to Monero, liquidity to a major L1 and its family of tokens, and of course, fast finality.

I assume there will be bridges to other chains so even if, say, USDT is not natively issued on Tempo you can bridge it.

It's Stripe, so maybe they are allowed to mint their own USD stable coin

Stripe has USDB. https://www.bridge.xyz/news/usdb

That being said, I'm not entirely sure it's a bad thing...especially outside of the US/europe banking I get the impression that banking regulations are arbitrary and political and if all we get from crypto is escape from those regulations it may be worth the extra fraud and so on.

There are some legitimate advantages of ethereum (multiple independent validator software implementations) but decentralisation of the L1 isn’t one of them, even more so when you consider most ethereum transactions happen over centralized L2s.

I did not see the mention of decentralised BTW, why would it matter here? You trust business entity at the end of the day.

I can hardly see any value in "yet another private blockchain" — just use a database, duh.

Most of these L1s will likely end up becoming L2s in the near future, especially if they can rake in revenue via sequencers

We're looking at stable coins for the following use cases:

1. Instant clearing and settlement of 'floats' & liquidity - EG moving liquidity between our network to support instant/same day payouts or instant funding of a spend card.

2. Instant cross border payments (lots of people doing this already in companies that operate multinationally). EG, our USD top-ups today take 3 days in fiat, which can cause operational issues.

3. Offering our merchants (who are typically small businesses) optionality to hold USD in countries that have volatile currencies.

I'll also note that many people forget that the cost of a payment network isn't merely the movement of money, it's also KYC, dispute resolution, fraud prevention etc...

I wonder if the tempo team has looked at AI automating dispute resolution and fraud detection/prevention 'on chain'.. The network could fund the compute required for the AI to complete these tasks.

Does this mean these companies are about to start accepting stablecoins as payment (via Tempo?) some time in the future? Seems out of the ordinary to work with these companies otherwise.

Wouldn't that just mean that the whole schtick is to avoid regulation? If I as a regulator saw this, I'd just schedule it for my next meeting, since you want to avoid having companies doing regulatory exploits "until regulation catches up". It's Uber all over otherwise.

Blockchains (in general) enforce not only open code, but open data.

Technically, nothing prevents traditional banks to offer standardized easy-to-use and easy-to-onboard API access to their financial data, but in reality incentives are not there (quite the opposite).

Blockchains are a contrived way to enforce open code and open data. There are other technical ways to do that, but none of them has been found to actually work in reality.

Sure, some people thought buying tokens was a way to become rich quick and lost money. Yes, some projects were not regulated and the regulators need to catch up. But overall progress is impressive imo.

I actually don't understand how they were allowed to exist, it's impressive really.

I'm cautious about these

If you can't make it economically viable, it shouldn't exist. Pure and simple.

they will censor you and block you in blockchain level so literally db for few big companies, lol.

Both of these are the antithesis to censorship resistance because not only are all transactions publicly tracable but also non-fungible making censorship not only possible but viable on a large scale.

https://cryptodefendersalliance.com/blacklist

Monero is actual censorship resistant currency.

https://www.getmonero.org/resources/moneropedia/fungibility....

So now it’s official? The other blockchains were designed for gambling?

Anyone know what this actually means? Both literally (what is Reth?) and what it means qualitatively: are Stripe’s crypto efforts competing with Ethereum or strengthening it?

Reth - ethereum protocol client written in rust. https://github.com/paradigmxyz/reth

Reth is a rust implementation of the EVM used for running nodes, made by a very prominent research and venture group.

Is this an actual public "blockchain"? Can anyone read it and archive all the transactions? Are there multiple validators who have to agree? Or is this really just a proprietary database?

> Attributes: High motor

What is meant by that?

[1] https://jobs.ashbyhq.com/tempo-xyz/aab97703-13e2-42e8-9fb9-9...

There’s a physicality in the definition that doesn’t really describe the best programmers I’ve worked with.

> In sports, "high motor" describes a player who consistently exerts maximum effort and intensity on every play, showing relentless energy, enthusiasm, and a refusal to take plays off, even when tired or the game situation is difficult.

Feeling defeated is important too to rethink your strategy.

Recruiters want Übermenschen probably.

In this day and age, countries need not be beholden to the pile of duct tape that is the credit card system and its innumerate middle-men and inefficiencies.

This is a good thing.

Something claiming over 20-30 tps onchain is usually a big blocker. Big blocker design is well recognized as insecure: no end user is able to run a full node locally, only datacenters are able to keep up with 100k tps load. Which diminishes entire purpose of creating a blockchain. Could have been a database with 100k tps or 3-of-4 validator multisig like Hyperledger, wouldn't matter.

> A diverse group of independent entities, including some of Tempo’s design partners, will run validator nodes initially before we transition to a permissionless model.

> Protect your users by keeping important transaction details private while maintaining compliance standards.

Sounds like it actually has potential. This could enable global QR-code payments using and open, decentralized, and private system. Something like fiat cash payments, but digital. I hope that Valve is keeping track of it, for starters.

In what currency? As I understand it, Stablecoins are bound to an underlying currency. If you do not wan't to tie it to a currency, bitcoin would be the prime candidate. And with its layer 2 solutions such as Lightning, there is already a decentralized system for fast, cheap and private payments.

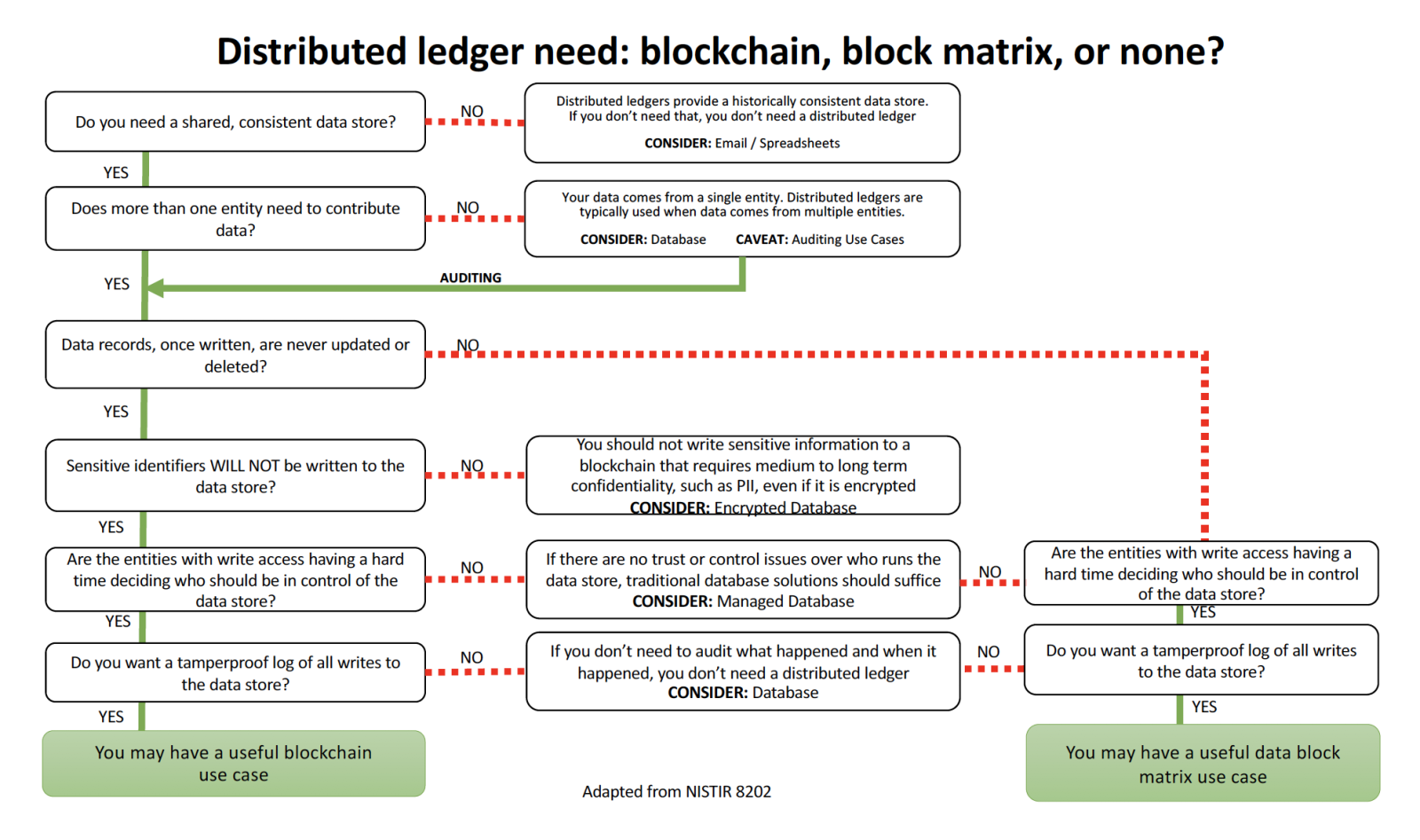

* https://www.nist.gov/blockchain

Specifically the yes/no flowchart on whether "you may have a useful blockchain use case" (Figure 6 - DHS Science & Technology Directorate Flowchart):

* https://csrc.nist.gov/CSRC/media/Projects/enhanced-distribut...

Once it's truly "open", you can't have any sensitive identifiers in there, so you need another protocol/system for correlating opaque identifiers with real-world entities (thus defeating the purpose).

And if financial institutions are involved, they'll want the ability to do what they do now: rewrite history whenever they feel the need (or are compelled by governments). Another strike against using blockchain.

"Are the entities with write access having a difficult time deciding who should be in charge of the data store"

The vast majority of pointless blockchaining come from organisations that have already decided that they are going to be in charge. Which is just great for them, but it doesn't induce others to join them. I wonder how much of promoting blockchains is to project the illusion of relinquishing a degree of control. I guess all the ones doing it just because others were doing it are looking at AI now.

Who would of thought?

Asked a crypto friend how to manage it in 2025, he pointed me to a service that I could use with Google Pay. Mental. I was just walking into normie places and paying with my ill-gotten gains.

It's gone mainstream for sure.

I wonder if that's intentional or left in from debugging the animation when it was being created. As-is felt like a nice easter egg and I appreciated it being included.

I do think it's possible they put more money/talent onto the problem after it happened though.

The one that really stands out to me is

“ 03 :: Predictable low fees

Transform your cost structure with near-zero transaction fees that are highly predictable and can be paid in any stablecoin.”

I question why some of large companies that are named here as partners would want this.

Being a Stripe customer from Country XY, charging my customers in USD and getting charged a hefty fee by Stripe for the conversion when I have a payout, I wonder how this would affect their business model.

For example, in markets like Latin America, stablecoins aren’t just ‘faster payments’—they’re an escape hatch from broken financial infrastructure. That makes them feel less like a new technology experiment and more like electricity or the internet: invisible, but transformative.

The interesting question to me is: what happens once small/medium businesses start building on top of this instead of just using it for payments? Could we see the same pattern as the early web—where it started as “publishing pages” but turned into entire industries?”

Regulations in payments tend to be very technical, and inserting some crypto/distributed plausible deniability in the mix could get them 5 more years of delay (until the next generation of regulations). It will depend on how those regulations take shape in the coming months.

> Stablecoins enable instant, borderless, programmable transactions, but current blockchain infrastructure isn’t designed for them: existing systems are either fully general or trading-focused. Tempo is a blockchain designed and built for real-world payments.

What is different in the details, no idea.

I can't see this as a positive because of how Stripe has behaved in terms of preventing transactions in the past. Although Tempo is behaving more like a b2b model or fintech-specific orgs in this case, the shoe-drop is when they decide a particular bank, or fintech org, or product is not allowed to perform the transaction on their network after the market capture takes place.

This sounds like a „private blockchain“, which loses a lot of the advantages to me, but, if designed correctly, it may still produce a very solid and long living platform if there are many parties interested in keeping it running.

Do consider me skeptical that Stripe will actually cede enough control for this advantage to materialize since that’s just not what companies are incentivized to do.

I run e-commerce business and I’ve received bullshit chargebacks before. But I’m also a consumer and I’ve filed legitimate chargebacks before.

Related: I’ve also had my bank send money to the wrong place before.

There must be some means of reversing transactions in some cases. Some arbitration mechanism. Some dispute resolution procedure. Some means of doing escrow.

You already have binance b2b and similar stuff that do escrow and it works ok

Can anyone answer this? (I'm not asking to be rhetorical or negative, just critical but inquisitive).

Tempo is a purpose-built, layer 1 blockchain for payments, developed in partnership with leading fintechs and Fortune 500s. With support for all major stablecoins, Tempo enables high-throughput, low-cost global transactions for any business use case.Yeah I can't wait to run my operations on a KYC-guarded, AML-choked blockchain in the US jurisdiction.

(and I'm saying that as a huge crypto/blockchain optimist)

Tether has now moved to Bukele's paradise El Salvador and its backing is managed by Howard Lutnick's Cantor Fitzgerald. Previously Tether's funds were managed by Deltec in the Caribbean, a bank with a colorful history.

https://www.ft.com/content/b3c5b67d-1df8-4417-8dd5-2c86d76d6...

For example, in markets like Latin America, stablecoins aren’t just ‘faster payments’—they’re an escape hatch from broken financial infrastructure. That makes them feel less like a new technology experiment and more like electricity or the internet: invisible, but transformative.

The interesting question to me is: what happens once small/medium businesses start building on top of this instead of just using it for payments? Could we see the same pattern as the early web—where it started as “publishing pages” but turned into entire industries?

There is no technological replacement for trust. To think otherwise is a bit daft.

All financial instruments are expressions of trust / promises or more informally known as IOU's.

I'm yet to see someone do a thorough economic analysis of how all this blockchain stuff will positive impact this.

I have no bias - please bring me well formed arguments. I want to see them!

TerraUSD (UST) NuBits DEI flexUSD

USD has been here all this time. And is a safer bet than any stable coin.

In my finance experience, the answer to the "why blockchain" question is settlement. Every banking system (local, international) has a settlement process.

Settlement is where bank counterparties have to tally up who owes whom, and pay each other. That process still takes time internationally, and is complex because of the parties involved.

A more concrete example (I've audited interbank settlements for a local bank in my country):

When I buy something from Amazon as a crossborder transaction with my Visa, my bank and the merchant/bank that Amazon use enter into a counterparty obligation, where in a direct way they'd have to pay each other, incl moving funds between countries. If these 2 banks are the only banks in the world, they can both tally up the transfer of funds to each other, and then pay each other the difference. That'd still take time, right?

Now, we have hundreds of counterparties, using different systems, Visa, MasterCard, Amex, local clearing houses for EFTs, etc. There's also merchants like Stripe who'll be doing the processing, central banks who also ultimately settle currencies among each other. They all have to wait for proof of funds clearing at some level.

If I'm doing an international transfer to my friend, their bank won't want to just credit their account instantly because the time it'll take for them to receive settlement of those funds isn't instant. Else they're going to pay the cost of a deposit that isn't there (let's assume my friend earns interest on positive balances).

The process is that the banks have to recon each clearing house's balance, aggregate that to a list of values like:

* Amex: owes us R200m * Visa: pay them R300m * Clearing house: etc.

Typically the bank's treasury department then effects those transfers. Don't know about other banks, but the bank I audited, it was done by a person daily, their responsibilities are to ensure those settlement aggregates are received/paid, and to resolve differences.

Beneath this person, at that bank, was a team of people who did recons all day. This was in 2012, so hopefully things changed, but I know that team still exists.

Once settlement's taken place, there's another team that verifies international settlements and then approves transfers to my local account. As a data point, it used to take me ~7 days to receive my salary from a US employer while in South Africa.

With crypto, my experience has been that settlement gets delayed, virtualised and distributed because you have a single layer (or still fewer layers across chains).

You send me USDC from wherever, we already don't involve:

* Payment processors like Visa * Central banks as no balance of payments processes are affected * Banks who need to reconcile cross-payments and settle them

Instead, if we're using an exchange (if you're using a local exchange), the funds arrive in the exchange's wallet shortly. The exchange has a constant flow of users buying and selling their local currency. They're in charge of settlement between their wallets and bank accounts.

I'll sell my USDC into my local currency ZAR, and if I withdraw it, the exchange keeps ZAR in local banks, and they send me that money immediately. My crypto salary would be in my bank as ZAR in 30-60 minutes.

Now, I said that crypto delays settlement. My exchange will eventually run out of fiat currency, or need to rebalance. They'll trade some other counterparty exchange, and settle that transaction through SWIFT/equivalent. That settlement will take the 5-7 day process. They just delayed it for their client.

I said it's virtualised because they've skipped the whole process of moving net flows and relied on a central entity, the blockchain, to do that. Ultimately it's a faster process than that backoffice of the bank.

And distributed. Every exchange or remitter has now become their own micro clearing house, and they participate in the banking system by earning their own fees, running their own process.

They only need to interact with each other at higher levels if they need to convert their USDC to US dollars. Interestingly that process happens at one place, but as long as cash and tokens move bidirectionally, the process can get relayed to the point where only a few US banks need to deal with the issuer of USDC.

Immovable object: The perennial HN hate for all things blockchain, complete TLDR energy when it comes to crypto

This should be interesting

1. We all desperately need a sane digital instant means of transferring money between “institutions” that just works

2. No-one believes that a third party solution would not end up with that third party holding everyone over a barrel (Visa but on steroids). So any simple “use Postgres” is out

3. So it’s either a trustless, open blockchain (bitcoins blockchain or possibly this Tempo). But there are huge drawbacks to The Blockchain - apart from the ratty reputation it has so far, there are problems with making a reversal of payment of both parties don’t agree, and other issues as nauseum.

I don’t get how well tempo solves any of this.

4. We end up with what I think is likely to be the solution(s). Islands of “trust groups” that replace SWIFT and its like with blockchain in a piecemeal fashion, but the cost benefit ratio is totally subsumed by the massively high costs of replacing the towers of process, regulation and software balanced on top of SWIFT etc

4.a. Or the central banks introduce their own “stablecoins ” - and people punt all the complicated bits of law and regulation and reversals over to the existing legal regulatory frameworks.

In short the ultimate problem is that sending a signal moving 1 million dollars from Kenya to Kansas is simple (wooden sticks did this a millennia ago).

The problem is a legal, cultural, social framework that all parties can trust and believe will fix their grievances. That’s basically … the global Legal framework we have now, with the solutions we have now including following court orders.

If the electronic system cannot follow the current frameworks requirements (ie the old lady did not mean to send her life savings to that wallet, get it back) then the electronic system still needs overlays that can - and there is not just a lot of complexity - there is an incredible amount of complexity

I get the feeling I’m yet again talking myself out of thinking we can have a sane digital currency for similar reasons to why we can’t vote electronically.

I’m paying for my round at the bar in cash.

Why does Stripe want to creatively ruin their reputation by venturing into crypto / blockchain?

I don't see anyone in the real world using blockchains at all.

I get AI as it was a real world paradigm shift, but I have never seen anything in this blockchain / crypto space that has reached 100-500 million users let alone 1 billion users, that isn't based on speculation.

People use it for selling accounts, usernames, cheats and probably much more for it. Many of these also use Stripe (major cheat providers offer payments via Stripe and crypto, so why shouldn't Stripe also try to capture the value of Crypto payments?).

Many companies are using stablecoins for cross border transactions, and for payouts in countries with volatile currencies. There's clear value for these use-cases.

Not to mention lower fees and 24/7 availability.

Ah yes, the good old "permissionless" blockchain, that's 100% centralized for just the first 100 years of operation, give or take [subject to updated timelines after 100 years]

https://coinmarketcap.com/charts/number-of-cryptocurrencies-...

Bitcoin is decentralized because the sun distributes energy somewhat evenly across the globe.

The other 206701340 crypto projects, including this one, are decentralized because ... ?

From the very sparse info on the page, it seems this project does what so many other chains do to make payments faster and cheaper: They log them on a database that is synchronized across only a few computers.

In other words: I can't find any info on that page explaining how they plan to achieve decentralization.

Second, permissionless does not mean decentralized. You can have all validation of a POS chain ending up on a single computer.

There are mild returns to scale in running large-scale mining operations and as a result mining power seems to actually be somewhat centralized under the control of a small number of players: https://digiconomist.net/cryptocurrency-decentralization/

Not to mention that "decentralization" is a technical property and not necessarily desirable in itself. Users might care about fairness, avoiding sanctions, purchasing illegal goods, etc, but these are only weakly connected to technical decentralization.

In March 2023, the New York Times identified a list of

just 34 Bitcoin mining facilities (controlled by 22

different entities) in the United States, which

represented about a third of the total worldwide

Bitcoin mining network at the time.

34 such $365M/year entities would have to collude to attack bitcoin. And accept that their business is severely damaged afterwards.

So much for the decentralization and security of Bitcoin.

How does the situation look like in other chains?

Good luck to Stripe though. Building the network effects necessary for an L1 is very difficult.

So not decentralized at all. The only reason to not open source validators and allow the public to run their own is to make insiders rich. Another crypto grift that will mint a few millionaires before either being forgotten or merely being used as a speculative instrument.

That says nothing of political idiocy which will surely follow as new levers are tested, but payment processors are in the business of making money, and ostensibly want as many transactions to happen as possible, regardless of origin or the particulars of any sale.

They shouldn't be gatekeeping goods and services for legal transactions, and I'd be willing to bet most of them absolutely don't want to be in that position.

I imagine there's also a chargeback scam reduction and accountability benefit to this, which reduces losses, and ostensibly prices.

There's a surveillance and privacy hit, but it's not like the systems currently being used aren't completely compromised and surveilled already, so maybe this adds some accountability at that level as well.

Stablecoins enable instant, borderless, programmable transactions, but current blockchain infrastructure isn’t designed for them: existing systems are either fully general or trading-focused. Tempo is a blockchain designed and built for real-world payments.

- First line in TFA

How?

> existing systems are either fully general or trading-focused. Tempo is a blockchain designed and built for real-world payments.

What makes existing systems not suitable for instant, borderless transactions? What makes this new chain suitable for instant, borderless transactions?

Any system with an API is programmable.

But I had literally said that stripe should've actually ventured into and created their own cryptocurrency or something...

Tada, I might be one of the happiest person thinking that I actually really predicted something by my own observations.

here's the blog post: https://justforhn.mataroa.blog/blog/most-crypto-is-doomed-to...

By what I meant most crypto, I meant anything aside from stablecoin (like gold backed/usd backed)

Now that being said, I am still a little critic as to I don't see any offical stripe message and I don't see a way on how it would be implemented?

Like one of the things that I wished in my article was this idea that someone on twitter originally asked where currently if you had money in stripe and wanted to pay it anywhere else, you had to have it enter your bank which might take 14 days and then lets say you want to give it to someone else who has stripe(think anthropic), then they would get it back again after 14 days

So someone basically asked to create something similar to a stripe card. I think that this blockchain is it, except I feel like that you could send money to anyone in a non kyc manner too via this which is again a plus point for sometimes where I feel like that in this world every transaction is usually tracked and as such something like this change is really welcomed.

Once again, can someone really explain what is going to happen in tempo's future as maybe its me who couldn't focus in such a website. I actually went and read the article that the other company that partnered with stripe (paradigm), so I just read paradigm's article: https://www.paradigm.xyz/2025/09/tempo-payments-first-blockc... and they say that it is a new incubator/partnership b/w stripe and them, but would that mean that this tempo is going to be integrated in the stripe ecosystem or no?

I always thought that stripe and stellar had some deep connections but honestly I couldn't care less about it. I don't care about these fake tokens but rather stablecoins/gold stablecoins

Eg if Australian locals suddenly switch transacting cocaine at scale in Tether instead of AUD, the US government can borrow more money by providing that collateral to Tether.

Edit: Izzy Kaminska recently had a, as always, solid and less snarky summary at https://www.financialsense.com/blog/21379/redollarization-an...

I honestly thought this was fake and not from stripe the first time I saw it. (I kinda still do with that domain.)

According to this Krebs article https://krebsonsecurity.com/2024/12/why-phishers-love-new-tl... 13% of the xyz domains was related to phishing, not as bad as .top which ahd 30% but still bad.

I would love for stripe to start paying appropriate VAT on transactions between their merchants and EU citizens, I've been on their ass about it for nearly a year now. I've reported multiple merchants to them which simply refused to provide an VAT invoice for any transactions. Legally, merchants outside EU are required to pay VAT on their B2C transactions if their EU transaction volume goes above a certain limit, and provide VAT invoice for B2B transactions (but with 0% VAT because it is B2B).

But unfortunately Stripe doesn't seem to have the technology to do a SUM(*) in their database, or check if an email address ends in '.de' or '.it' when they take the payment. So they simply do not give a damn if their merchants provide an invoice with the transaction or not.

Oftentimes it was the problem to actually get an invoice document which has company name, company registration number, street address, city, and tax ID. Extremely basic information which is required on all EU invoices. Many times I have submitted invoices from Stripe merchants to my tax accountant and my tax accountant told me that those are not proper invoices and to please reach out to the merchant to get EU-legal invoices.

Stripe has the technological capabilities to implement proper compliance checks, but they choose to let their merchants send you rubbish self-made PDF invoices with a big red "paid" stamp without any information or "official" Stripe invoices with total fantasy names and fantasy company information. You never know if your merchant is sitting in an embargoed country or is just some schmuck from San Francisco trying to hide their ties to a website.

If other HN users from the EU have been fighting Stripe to get EU-compliant VAT invoices for their B2B or B2C purchases, please feel free to reach out. I've been doing a big stink about this and to me it feels like a deliberate pattern of enabling their merchants to ignore EU VAT obligations.

It's really sad that my extremely positive impression of Stripe has been deeply tainted by this kind of experience across various purchases and subscriptions with Stripe merchants. I had to spend so much time pleading with them to provide proper invoices.

You're trying to get Stripe to force merchants to conform to some arbitrary document format for an invoice that isn't even part of Stripe's transaction flow, based on a regex on emails for certain TLDs?? Is Stripe the world's paperwork policeman?

Maybe just don't order from merchants who won't supply you documents in the format you like, instead of trying to get Stripe to act as judge, jury, and executioner in the court of Stripe. Or talk to your government representatives and get them to lift these rules so you can do business like everyone else in the world.

So if Stripe doesn't force their merchants to provide an invoice which has company name, company address (jurisdiction!) and company registration number (for me to check if it actually exists) then the invoice is rubbish and to be used as toilet paper.