So yeah, money becoming less of a proxy of "how much someone contributed to society" and more "how much someone contributed to the oligarchs' goals", while those goals are for AI and for peoples' detriment, makes the situation actually about AI.

The technology that helps extract wealth improves, while most of the purely consumer-oriented products are becoming a con and a scam, especially if US companies are involved. The Mirabell's "original" recipe turned the best treat in the world into a generic candy, all are just palm oil + sugar + shrinkflation. There is also non-repairable tech with non-standard components, non-removable batteries, meat gets filled with water, washing machines die right after warranty ends, every digital service is trying to steal data instead of taking only the necessary or at least being transparent about what's taken and why, entertainment like Reddit and streaming services also get worse... AI slop is just another example, but a bit more visible and with a bit more side-effects.

This seems like the polar opposite of what the "AI safety" people are worried about and it seems unlikely that they could both be true at once.

> As I understand it, the last sentence stems from the fact that too large of a share of the total wealth is in the hands of those that don't benefit from more homes. AI is what's prioritised by them and what will lead to even smaller flow from the efficient wealth aggregators to those needing homes

These are both two independent things and two independent sets of people.

The main group of people opposing housing construction is landlords and existing homeowners. The ones doing AI have almost no overlap with that. Moreover, "you get paid less" and "housing costs more due to artificial scarcity" are only tied together in the sense that money going to landlords and banks isn't going to workers, which again isn't the AI thing.

Or to put it a different way, you could mitigate a lot of the "AI problems" by building more housing and the AI people would be pretty fine with that.

Alex Karp, in particular, has some of the most absolutely horrifying clips of his TV appearances circulating all over video social media. But Musk has broader reach, and is even more oblivious and has tied himself to someone who he himself accused of pedophilia.

Andreesen, Thiel, Sam Altman, and the above are great at raising valuations for investors but they are doing it incredibly stupidly in a way that leads to massive backlash. California is voting for a billionaire tax this year, and I think that these tech CEOs only have themselves to blame for the backlash they are causing.

The problem isn't that these people are simply inarticulate and incapable of expressing their views in ways that appeal to people. It's that their views are unappealing (if not downright objectionable) to most people.

It's a sign of how disempowered the populace is that these selfish ghouls don't even feel the need to pretend to be decent functioning adults anymore. Because, why bother? What is anyone gonna do about it?

I bet you there are people equally repulsive and influential but face little public backlash because they never show up in front of a camera.

Notice that all these countries are English speaking countries? Aside from speaking English they also have lots in common when it comes to the way the economy and society is run. I can only speak for the United States, but I’ve noticed unfordable not luxury apartments going up everywhere and starter homes are not.

But the real villains here are the same as ever, the most dangerous non-human persons: corporate persons.

The economy, real wages, etc are basically higher than ever (despite idiot Trump's best efforts).

People are mad because being mad is fun and we're all on being mad machines 24/7.

Hopefully non-logged in users can at lease see the income-by-age graph: https://www.economist.com/cdn-cgi/image/width=480,quality=10...

https://prospect.org/2024/05/14/2024-05-14-trendy-nonsense-g...

> The Economist piece and kindred articles are good examples of how to lie with statistics. You can show that the typical 25-year-old’s income outpaces boomers’ income when they were 25 only by failing to adjust for inflation and the rising costs of life’s necessities, or using averages rather than medians.

But the Economist did use inflation-adjusted median earnings in its analysis of incomes by age among different generations. The Economist cited the median after-tax income, adjusted for inflation. (https://www.economist.com/cdn-cgi/image/width=600,quality=10...) I'm not sure why this author seems to think that the Economist is failing to adjust for inflation or not using medians, when it says so quite clearly in their graphs.

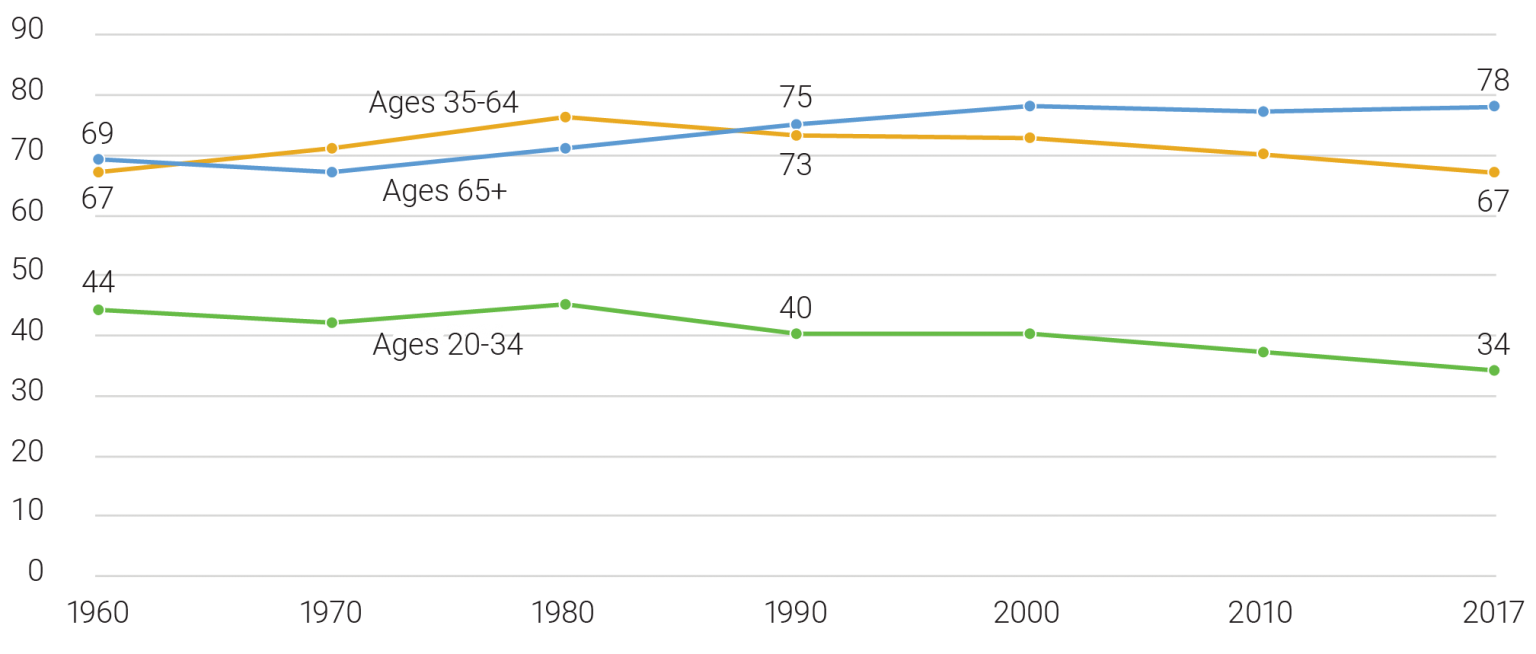

The Prospect article also says that home ownership among under-35s has gone down, and links to data on the home ownership rates grouped by age (https://www.prb.org/wp-content/uploads/2020/02/a-02132020-ar...) but the data ends in 2017. The oldest of Gen-Z would only be 20 years old at the time this data ends. When we look at the Economist's wrote:

> Bolstered by high incomes, American Zoomers’ home-ownership rates are higher than millennials’ at the same age (even if they are lower than previous generations’).

A chart of home ownership rates that end in 2017 could not possibly refute this claim given that Gen-Z would be too young to buy homes around the time that the data's source ends. The home ownership rate among under-35s increased from 34% in 2017 to 39% in 2023 (https://www.census.gov/library/stories/2023/07/younger-house...), so when Gen-Z started to enter their earliest feasible home-buying years the ownership rate was in a period of recovery. The Economist's claims seem to bear out.

The rest of the piece goes off on tangents largely unrelated to the financial outcomes related to Gen-Z relative to previous generations. For instance, it cites a pew survey on the percentage of young adults that support their parents. But it does not compare that against earlier decades, so there's no evidence in any change in rate over time. In fact the bulk of the piece shares data that aren't relevant. E.g. how does the racial breakdown of the subprime mortgages relate to incomes by age and birth year?

{kind=link}

{kind=link}

{kind=link}